Understanding health insurance deductibles and out-of-pocket maximums is absolutely crucial. Indeed, these terms often present a significant challenge. Many new investors find them confusing. Grasping these fundamental concepts, however, empowers you greatly. You can then navigate the complex world of healthcare financing. Consequently, this understanding directly impacts your financial well-being. It helps you make sound decisions. Therefore, this comprehensive guide aims to clarify both concepts. We will explain precisely how they impact your healthcare costs. Thus, you can choose the best health insurance plan with confidence and clarity. This knowledge will serve as a vital tool.

What is a Deductible?

Firstly, let’s precisely define a deductible. A deductible represents a specific monetary amount. You must personally pay this amount. It applies to covered healthcare services. This payment occurs before your health insurance plan initiates its contributions. For instance, consider a scenario where your deductible is set at $2,000. You would be responsible for paying the initial $2,000. These payments cover your medical bills directly. Specifically, this financial responsibility is incurred within a defined policy year. Only after your total out-of-pocket payments reach $2,000 does your insurer begin to contribute. Consequently, they then commence sharing the costs with you. This initial threshold is a critically important step. It fundamentally dictates your upfront financial responsibility each year.

However, it is vital to note that not all services count towards meeting this deductible. Preventive care, for example, is very often exempt from this requirement. Many modern health plans actually cover preventive services fully. This happens even before you meet your specified deductible. Therefore, routine annual check-ups, immunizations, and certain screenings usually incur no cost. This policy proactively encourages consistent health management. Furthermore, understanding what specific services do count towards your deductible is absolutely key. Always diligently check your specific policy documents. Indeed, these crucial details can vary significantly from one plan to another. Some plans also offer the option of lower deductibles. These choices typically come with correspondingly higher monthly premiums. Conversely, selecting a higher deductible often results in lower monthly premiums. This essential financial trade-off is absolutely vital for effective personal budgeting and long-term financial planning.

Moreover, consider the various structures of deductibles. An individual deductible applies specifically to one person within a plan. A family deductible, conversely, covers multiple members listed on the same policy. Once the aggregated family deductible is met, the insurance plan begins paying. This applies for all covered family members for the remainder of the policy year. Thus, it effectively pools expenses across the household. Furthermore, some plans implement separate deductibles. These might apply specifically for prescription drugs. They could also apply for out-of-network specialist visits. Always meticulously verify these specific provisions in your plan. Knowing these intricate nuances proactively prevents unwelcome financial surprises. This knowledge empowers smarter healthcare consumption decisions.

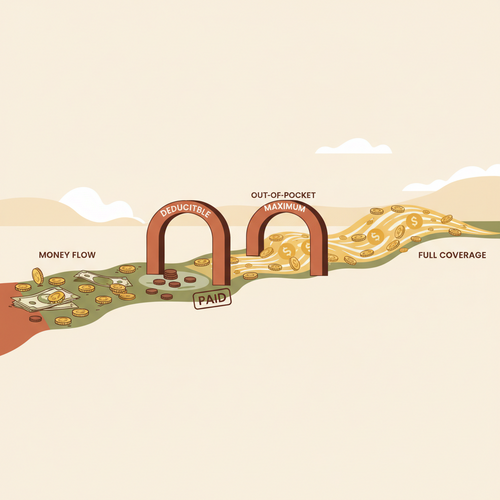

What is an Out-of-Pocket Maximum?

Now, let’s comprehensively discuss the out-of-pocket maximum. This critical limit is often referred to as the out-of-pocket limit. It fundamentally represents the absolute most money. You will personally pay for covered services within a defined policy year. Specifically, once your total eligible expenses reach this predetermined limit, your insurance plan then pays 100% of all subsequent costs. Therefore, your insurer fully covers all remaining medical expenses. These costs must, of course, be for services explicitly defined as covered benefits by your plan. This full coverage continues for the entire remainder of that policy year. This ultimate limit robustly protects you. It effectively prevents the burden of catastrophic medical bills. Consequently, it offers a profoundly significant layer of financial security.

Indeed, this maximum cap inclusively encompasses several different types of costs. Your annual deductible inherently counts towards it. Copayments for doctor visits and prescriptions also directly contribute. Coinsurance payments, where you share a percentage of the cost, are explicitly included too. However, it is crucial to understand that your regular monthly premiums do not count towards this maximum. Likewise, services that are explicitly not covered by your specific plan do not contribute. For instance, purely cosmetic surgery is typically excluded. Understanding precisely what contributes and what does not is paramount. It substantially helps you accurately track your healthcare spending. Furthermore, it clearly highlights the ultimate financial safety net provided by your plan. This cap serves as a critical, protective layer. It is especially vital during periods of serious illness, unforeseen accidents, or chronic conditions.

For example, imagine your plan’s out-of-pocket maximum is set at $8,000. You would first pay your $2,000 deductible. After meeting that, you would continue paying copays and coinsurance percentages. You persist with these payments until your cumulative total reaches $8,000. Once you hit that $8,000 threshold, you pay absolutely nothing further. Your insurance plan then covers 100% of all subsequent covered medical care. This continues until the policy year officially ends. Consequently, you gain invaluable peace of mind. Your financial exposure for medical costs is definitively capped. This level of predictability is incredibly invaluable for effective financial planning. Conversely, without this essential limit, medical costs could theoretically escalate indefinitely, posing an immense financial risk.

Deductibles vs. Out-of-Pocket Maximums: The Relationship

Understanding the intricate relationship between these two terms is absolutely key. The deductible serves as the initial financial hurdle. You must clear this specific amount first. Only then does your health insurance provider begin to pay its share. However, after the deductible, the plan usually pays only a percentage of costs. This cost-sharing arrangement is widely known as coinsurance. Therefore, you continue to share medical costs with your insurer. This ongoing cost-sharing phase continues. It lasts specifically until you reach the predetermined out-of-pocket maximum. Consequently, the out-of-pocket maximum functions as the ultimate financial ceiling. It unequivocally represents your absolute highest annual expense. This applies exclusively to covered services within the policy year.

For instance, let’s consider a clear financial scenario. Imagine your health insurance deductible is $2,000. Your corresponding out-of-pocket maximum is set at $8,000. You unfortunately experience a costly medical event, such as a significant surgery. You would first pay the initial $2,000 out of pocket. This payment successfully meets your annual deductible. Then, for subsequent covered services, your plan might pay 80%. You would then be responsible for paying the remaining 20%. This 20% is your coinsurance share. You continue making that 20% payment. This lasts specifically until your total cumulative payments reach $8,000. Once you hit that $8,000 mark, you pay absolutely nothing further for covered services. Your insurer then covers 100% of all subsequent medical costs. This continues until the current policy year ends. Thus, the out-of-pocket maximum genuinely caps your financial liability. Learn more about financial planning strategies.

Indeed, both these figures are critically important components. They collectively define your overall financial risk related to healthcare. A plan featuring a higher deductible typically means a correspondingly lower monthly premium. Conversely, a plan with a lower deductible often means a higher recurring monthly premium. However, the out-of-pocket maximum is equally, if not more, significant. It definitively determines your absolute worst-case financial scenario for the year. When diligently comparing various health insurance plans, always thoroughly evaluate both figures. Do not make the common mistake of focusing solely on just one. Both ultimately contribute to your total potential healthcare expenses. Therefore, adopting a holistic and comprehensive view is absolutely essential. This integrated approach significantly helps in making a truly informed choice. It ensures your plan genuinely aligns with your individual financial risk tolerance and health needs.

Examples to Illustrate

Example 1: Low Medical Costs

Sarah has a health insurance plan. Her individual deductible is $1,500. Her annual out-of-pocket maximum is $5,000. Throughout the year, she only has a few routine doctor visits and a minor prescription. Her total eligible medical bills amount to $1,000. Sarah directly pays the full $1,000 for these services. This amount successfully contributes towards her deductible. However, she does not fully reach her $1,500 deductible threshold. Therefore, her insurance does not yet begin to pay for these services. She pays nothing more than this $1,000 for the remainder of the year. Her total spending is precisely $1,000. This amount remains below both her deductible and her out-of-pocket maximum. Her financial exposure remains limited and predictable. Stay updated with global economic and health news.

Example 2: Moderate Medical Costs

John’s health plan features a $2,500 deductible. His annual out-of-pocket maximum is set at $7,000. In a particular year, he unfortunately incurs $4,000 in medical bills due to an unexpected injury. John first pays $2,500 out of pocket. This action successfully meets his annual deductible. The remaining $1,500 in medical bills is now subject to his plan’s coinsurance. His insurance plan covers 80% of these remaining costs. Consequently, John is responsible for paying the remaining 20% of $1,500. This equals an additional $300. His total payment for the year is $2,500 (deductible) + $300 (coinsurance) = $2,800. This cumulative amount is still below his $7,000 out-of-pocket maximum. His insurer, however, pays $1,200 (80% of $1,500) for the remaining bill portion. Thus, John’s exact financial responsibility is clearly defined and manageable.

Example 3: High Medical Costs

Maria faces significant, ongoing health issues that require extensive care. Her plan’s deductible is $3,000. Her annual out-of-pocket maximum is $8,000. Over the course of the year, her total eligible medical bills accumulate to $20,000. Maria initially pays her full $3,000 deductible. After this, her plan typically pays 80% of subsequent costs. She, therefore, pays 20% (coinsurance) of these ongoing charges. This cost-sharing continues diligently until her total cumulative out-of-pocket payments reach $8,000. Once she definitively hits this $8,000 threshold, she pays absolutely nothing else for covered services. The insurance provider then covers 100% of all the remaining $12,000 in medical costs. Consequently, her absolute maximum payment for that entire policy year is capped at $8,000. This critical limit robustly protects her from truly crippling and open-ended medical expenses. Access official tax information and healthcare related guidance.

Choosing the Right Plan

Selecting the most appropriate health insurance plan requires careful and strategic thought. Critically consider your expected future healthcare needs. Are you generally in excellent health, anticipating only infrequent doctor visits? Or do you realistically anticipate more frequent medical needs, perhaps including ongoing prescriptions or specialist appointments? Your honest answers to these questions should fundamentally guide your choice. For generally healthy individuals, a high-deductible health plan (HDHP) might be a financially suitable option. These plans frequently boast lower monthly premiums. However, they inherently carry a higher initial out-of-pocket risk for medical events. Conversely, if you realistically expect numerous medical needs throughout the year, a plan with a lower deductible could prove to be a far better financial fit. These plans typically feature higher monthly premiums but offer much lower initial out-of-pocket costs when you need care. Read insightful financial market analyses and personal finance tips.

Furthermore, always meticulously evaluate the specific out-of-pocket maximum associated with any plan. This figure is unequivocally crucial. It precisely defines your absolute worst-case financial scenario for the policy year. A lower out-of-pocket maximum inherently provides greater financial security and predictability. However, this enhanced security often correlates with correspondingly higher monthly premiums. Conversely, a plan with a higher out-of-pocket maximum generally translates to lower monthly premiums. You must thoughtfully balance this critical financial trade-off. Your personal comfort level with financial risk significantly matters in this decision. Therefore, diligently review all aspects of a prospective plan with meticulous care. Do not make the common mistake of solely focusing on the monthly premium amount. Consider the entire comprehensive cost structure. This includes deductibles, copayments, coinsurance, and, crucially, the out-of-pocket maximum. This holistic perspective ensures you make a truly informed and financially prudent choice. Explore government healthcare options and subsidies available to you.

Moreover, it is absolutely essential to thoroughly understand network restrictions. Utilizing in-network healthcare providers invariably costs less. Conversely, seeking care from out-of-network providers almost always results in higher costs. In some plans, expenses incurred from out-of-network care might not even count towards your annual out-of-pocket maximum. Always meticulously verify these intricate details within your plan documents. Confirm if your preferred doctors, specialists, and hospitals are explicitly considered in-network. This proactive step prevents highly unwelcome and unexpected balance billing. Specifically, clearly understand the distinction between individual and family out-of-pocket limits. Family plans very often incorporate both. Knowing these crucial distinctions is vital. It profoundly impacts your overall household budgeting and healthcare expenditure. Thus, thorough and diligent research before enrollment is truly indispensable for optimal financial protection.

Conclusion

In summary, both health insurance deductibles and out-of-pocket maximums are absolutely fundamental. They truly serve as the critical cornerstones of effective health insurance coverage. A deductible essentially represents your initial financial payment hurdle. Your insurance provider only commences paying its share after this initial amount is met. However, the out-of-pocket maximum stands as your ultimate financial safety net. It definitively caps your annual spending for covered medical services. Grasping these complex but crucial concepts truly empowers you. You can confidently and intelligently navigate the often-intimidating world of health insurance. Therefore, by understanding these mechanics, you robustly protect both your physical health and your vital financial well-being. Always diligently compare various insurance plans. Make choices that are precisely aligned with your unique personal circumstances and financial goals. This meticulous approach ensures comprehensive coverage and, most importantly, enduring financial peace of mind.