Introduction

Navigating the complex world of personal finance often involves critical decisions. One such decision centers on life insurance. Understanding its role is paramount for securing your financial future. Many individuals seek ways to protect their loved ones. They also aim to preserve their wealth for generations. This pursuit leads to a fundamental choice: Term vs. Whole Life Insurance. Both options offer distinct benefits. However, they also come with specific considerations. Making the right choice requires a deep analysis. This article provides a comprehensive guide. We will explore each type of policy in detail. Our goal is to empower you with knowledge. You can then make an an informed decision.

Life insurance is more than just a safety net. It is a cornerstone of robust financial planning. It impacts your investment strategies. It also influences your retirement goals. The policy you select affects your overall wealth protection. Therefore, a thorough understanding is essential. This analysis will clarify common misconceptions. It will highlight key features. By the end, you will grasp the nuances. You will be better equipped to choose. Your decision will align with your unique financial journey.

Understanding Term Life Insurance

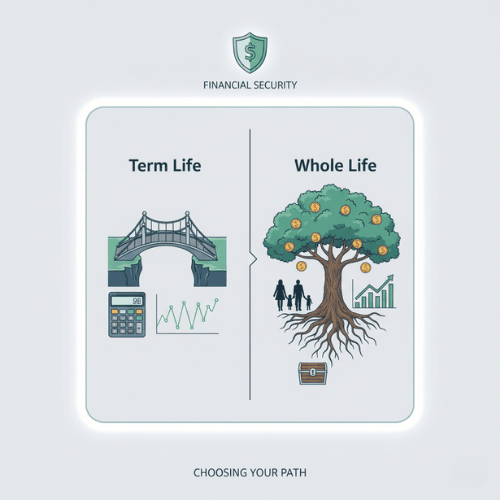

Term life insurance offers coverage for a specific period. This duration is called the “term.” Common terms include 10, 20, or 30 years. If the insured passes away during this time, a death benefit is paid. This benefit goes to designated beneficiaries. It provides crucial financial security. Term life is ideal for temporary financial obligations. Examples include mortgage payments or raising children. Its simplicity and focused protection are key features. This makes it a popular choice for many families.

The core of term life insurance is its pure protection. It does not accumulate cash value. Therefore, it lacks savings or investment components. Premiums are generally lower than whole life policies. This affordability allows for substantial coverage amounts. Premiums typically remain level throughout the policy term. After the term ends, renewal is an option. However, renewal premiums will be significantly higher. This increase reflects the insured’s advanced age. It also accounts for potential health changes. Term life is a straightforward solution. It addresses specific, time-limited needs effectively.

Key Features and Benefits

- Defined Coverage Period: Protection for a set number of years.

- Pure Death Benefit: Focuses solely on providing financial support upon death.

- Cost-Effective: Generally offers lower premiums for higher coverage.

- Predictable Premiums: Premiums usually stay consistent for the term.

- Flexibility: Can align with temporary financial responsibilities.

Considerations for Term Life

While affordable, term life insurance has limitations. Its coverage is not permanent. It ends after the specified term. If you outlive the policy, no benefit is paid. You might need to buy a new policy later. This new policy will come with higher costs. Term life also lacks a cash value component. It does not build wealth over time. You cannot borrow against it. There are no withdrawal options. For those seeking long-term savings or investment features, term life may not be sufficient. It serves as an excellent temporary safety net. However, it does not function as an asset-building tool.

Understanding Whole Life Insurance

Whole life insurance stands as a type of permanent life insurance. It provides coverage for the insured’s entire life. As long as premiums are paid, the policy remains active. This offers lifelong financial protection. A death benefit is guaranteed for beneficiaries. This permanence is a significant distinction. It sets whole life apart from term policies. It is designed for long-term wealth protection. It also serves estate planning goals. Many consider it a foundational element of a comprehensive financial plan.

Beyond its lifelong coverage, whole life insurance includes a cash value component. This cash value grows over time on a tax-deferred basis. It builds equity within the policy. Policyholders can access this cash value. Options include borrowing against it. They can also make withdrawals. The cash value growth is guaranteed. It also offers a fixed interest rate. This makes it a stable, predictable asset. Premiums for whole life policies are generally higher. This reflects the permanent coverage. It also covers the cash value accumulation. However, these premiums typically remain level for life.

Key Features of Whole Life Insurance

- Lifelong Coverage: Provides protection for the insured’s entire life.

- Cash Value Accumulation: Builds a guaranteed cash value over time.

- Guaranteed Death Benefit: Ensures a payout upon the insured’s death.

- Level Premiums: Premiums remain consistent throughout the policy’s life.

- Access to Cash Value: Policyholders can borrow or withdraw from the cash value.

Advantages of Whole Life Insurance

Whole life insurance offers numerous advantages. Its permanence ensures that loved ones will receive a death benefit. This provides peace of mind. The guaranteed cash value growth is a significant benefit. It acts as a stable savings component. This part of the policy is not subject to market volatility. Policyholders can use the cash value as an emergency fund. They can also fund education or retirement. It offers a unique form of liquidity. The predictable nature of whole life appeals to many. It integrates well into long-term financial strategies. It supports estate planning objectives effectively. It is a robust tool for wealth protection across generations.

Disadvantages of Whole Life Insurance

Despite its benefits, whole life insurance has some drawbacks. The most notable is its higher premium cost. These policies are considerably more expensive than term life insurance. This can make them less accessible for some budgets. The returns on cash value growth can be modest. They often lag behind other investment opportunities. This is especially true for market-based investments. The initial years of a whole life policy see slow cash value growth. A significant portion of early premiums goes to commissions and fees. Policy loans also incur interest. If not repaid, they can reduce the death benefit. These factors require careful consideration. They impact the overall financial efficiency of the policy.

Key Differences: Term vs. Whole Life Insurance

The choice between Term vs. Whole Life Insurance hinges on understanding their fundamental differences. These distinctions impact costs, flexibility, and long-term financial implications. Evaluating these aspects is crucial. It helps individuals align their insurance choice with their financial goals. Both policy types aim for wealth protection. However, they achieve it through different mechanisms. This section clarifies those contrasting approaches.

Coverage Duration

The most obvious difference lies in coverage duration. Term life insurance provides coverage for a specific period. This could be 10, 20, or 30 years. Once the term ends, coverage ceases. Whole life insurance, conversely, offers permanent coverage. It lasts for the insured’s entire life. As long as premiums are paid, the policy remains in force. This distinction dictates whether your protection is temporary or lifelong.

Cash Value Component

Another major difference is the presence of cash value. Term life policies are pure insurance. They do not build any cash value. They focus solely on the death benefit. Whole life policies accumulate cash value. This value grows guaranteed over time. It offers a savings component. Policyholders can access this cash value. This provides a financial resource during their lifetime. It is a key feature for long-term financial planning.

Premium Costs

Premiums vary significantly between the two types. Term life insurance is generally more affordable. Its lower premiums make substantial coverage accessible. This is especially true for younger individuals. Whole life insurance premiums are notably higher. This higher cost reflects its permanent nature. It also accounts for the cash value component. However, whole life premiums are typically level for life. Term premiums may increase dramatically upon renewal.

Flexibility and Purpose

Their design dictates their flexibility and purpose. Term life is best for specific, temporary needs. It covers obligations like mortgages or childcare. It is a cost-effective solution for a defined period. Whole life serves permanent needs. It is suitable for lifelong financial security. It supports estate planning and wealth transfer. Its cash value offers a unique investment-like feature. The choice depends on your specific financial timeline and goals for wealth protection.

Comparison Table: Term vs. Whole Life Insurance

Here is a concise comparison:

- Coverage: Term (Temporary) vs. Whole (Permanent)

- Cash Value: Term (None) vs. Whole (Accumulates over time)

- Premiums: Term (Lower, potentially increasing at renewal) vs. Whole (Higher, level for life)

- Investment Component: Term (None) vs. Whole (Guaranteed cash value growth)

- Flexibility: Term (Good for temporary needs) vs. Whole (Good for lifelong and estate planning)

- Borrowing/Withdrawals: Term (No) vs. Whole (Yes, against cash value)

Integrating Insurance with Your Financial Plan

Choosing between Term vs. Whole Life Insurance is not an isolated decision. It should integrate seamlessly with your broader financial plan. Your insurance strategy impacts investments, retirement savings, and estate planning. A well-chosen policy enhances your overall wealth protection. It ensures your financial goals remain achievable. This integration requires a holistic view. It considers all aspects of your financial life. Understanding this connection is vital for long-term success.

Considering Your Life Stage and Goals

Your current life stage plays a crucial role. Young professionals with dependents might prioritize affordable, high coverage. Term life insurance often fits this need perfectly. It covers immediate risks like a mortgage or children’s education. As you approach retirement, needs change. You might have fewer dependents. Your assets may have grown substantially. At this point, whole life insurance might offer advantages. Its cash value can supplement retirement income. It can also provide a tax-efficient legacy. The policy adapts to evolving financial landscapes. This flexibility is key to effective planning.

Impact on Investment Strategies

The choice of life insurance affects your investment capital. Lower premiums from term life free up funds. These funds can then be directed towards other investments. You might invest in stocks, bonds, or real estate. This strategy is often termed “buy term and invest the difference.” It allows for potentially higher investment returns. Whole life insurance, with its cash value, acts as an investment. However, its returns are typically more modest. It offers stability and guarantees. It often serves as a conservative component. It diversifies your overall portfolio. Both approaches have merits depending on risk tolerance.

Retirement Planning and Estate Considerations

Life insurance is a powerful tool for retirement planning. It also aids in estate considerations. A whole life policy’s cash value can supplement retirement income. It offers a non-correlated asset. This adds stability to your retirement portfolio. For estate planning, a guaranteed death benefit is invaluable. It can cover estate taxes or provide for heirs. Term life insurance provides a death benefit too. It ensures financial support if you pass away prematurely. This protects your family during critical years. It ensures they meet financial obligations. Both types of insurance contribute to a secure financial legacy. They offer different paths to wealth protection and transfer.

Professional Guidance

Navigating these complex decisions can be challenging. Seeking advice from a qualified financial advisor is highly recommended. An advisor can assess your unique situation. They consider your income, debts, dependents, and goals. They help you understand the fine print of each policy. This professional guidance ensures your choice aligns perfectly. It integrates with your overall financial strategy. Such advice helps maximize your wealth protection. It also optimizes your financial future.

Conclusion

The decision between Term vs. Whole Life Insurance is a pivotal one. It significantly shapes your financial security. Both policies offer unique advantages. They also present distinct considerations. Term life insurance provides affordable, temporary coverage. It is ideal for covering specific, time-bound financial needs. It allows for greater flexibility. You can invest the premium difference elsewhere. This strategy potentially yields higher returns. It is a practical solution for many families. It provides peace of mind during critical life stages. However, its lack of cash value and finite term are important factors. These should be weighed carefully in your financial planning.

Conversely, Whole life insurance offers permanent coverage. It includes a guaranteed cash value component. This policy acts as a stable asset builder. It provides lifelong protection. It supports estate planning and wealth transfer. Its predictable growth and borrowing options offer unique benefits. While more expensive, it integrates as a conservative investment. It diversifies your overall financial portfolio. Ultimately, the best choice depends on individual circumstances. It hinges on your specific financial goals. Your budget and long-term vision are also crucial. Thorough research is essential. Consulting with a financial professional is advised. This ensures an informed decision. The right insurance policy is a cornerstone of effective wealth protection. It secures your financial future for years to come.