Quick Summary:

- 🚗 Liability insurance covers damage you cause to others.

- 🛡️ Comprehensive insurance protects your car from non-collision incidents.

- 🧠 Choosing wisely depends on your car’s value and budget.

Navigating the world of auto insurance can feel overwhelming, especially when you encounter terms like “liability” and “comprehensive.” Don’t worry, you’re not alone in feeling confused by the jargon.

Many drivers, myself included, have stood at the crossroads of deciding which coverage is truly necessary. Understanding these two core types of insurance is crucial for protecting your finances and your peace of mind on the road.

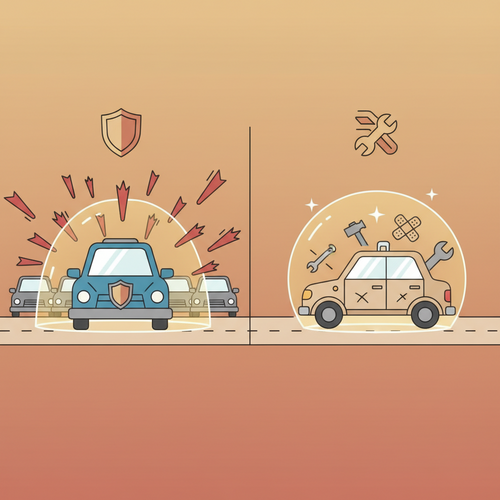

What is Liability Auto Insurance?

Imagine you’re involved in an accident, and it’s your fault. Liability insurance steps in to cover the costs for the other party’s damages and injuries. It’s designed to protect *them* from *your* mistakes, not your own vehicle.

Most states mandate a minimum level of liability coverage, making it a legal requirement to drive. This ensures that if you cause an accident, the victims have a means to cover their medical bills or car repairs.

Pro Tip: Always check your state’s minimum liability requirements. While meeting the minimum is legal, it might not be enough to fully protect your assets if a serious accident occurs.

Understanding the Two Parts of Liability

Liability insurance typically has two main components: bodily injury liability and property damage liability. These cover different aspects of the harm you might inflict on others in an accident.

Bodily injury liability covers medical expenses, lost wages, and pain and suffering for others involved in an accident you cause. This is crucial because medical costs can quickly skyrocket after even a minor incident.

On the other hand, property damage liability pays for repairs or replacement of another person’s vehicle or property if you’re responsible for the damage. Think fences, mailboxes, or even buildings – if your car hits it, this coverage helps.

- 📝 Bodily Injury (BI): Covers medical bills and lost income for others.

- 💰 Property Damage (PD): Pays for repairs to other people’s cars or property.

- 📍 State Mandated: Usually a legal minimum to drive.

What is Comprehensive Auto Insurance?

Now, let’s switch gears to comprehensive insurance. Unlike liability, comprehensive coverage protects *your* car from events that aren’t collisions. It’s your safety net for the unexpected.

This includes incidents like theft, vandalism, fire, natural disasters (hail, floods), and even hitting an animal. In my experience, many drivers appreciate this coverage during extreme weather events or if they live in areas prone to specific risks.

Warning: Comprehensive insurance does NOT cover damage from hitting another vehicle or object (that’s collision) or injuries to yourself/passengers (that’s medical payments/PIP). Understand its specific scope.

Common Comprehensive Claims

I’ve seen firsthand how comprehensive coverage can be a lifesaver for many. For instance, if a tree branch falls on your car during a storm, or if your vehicle is stolen from your driveway, this policy helps cover the repair or replacement costs.

It’s important to remember that comprehensive claims often have a deductible, just like other types of insurance. You’ll pay this amount out of pocket before your insurance company covers the rest of the damages.

Consider the value of your car when deciding on comprehensive coverage. If your vehicle is older and has little market value, the cost of the premium might outweigh the potential payout.

The Key Differences: Liability vs. Comprehensive

To truly understand what you need, it’s essential to see these two coverages side-by-side. They serve fundamentally different purposes, yet both contribute to a robust insurance plan.

Liability is about protecting others from your actions, while comprehensive is about protecting your car from external, non-collision events. They are distinct but often complementary parts of a full auto insurance policy.

| Feature | Liability Insurance | Comprehensive Insurance |

|---|---|---|

| What it covers | Damage/injury you cause to others. | Damage to your car from non-collision events. |

| Who it protects | Other drivers/property owners. | You and your vehicle. |

| Common incidents | At-fault collisions, property damage. | Theft, vandalism, fire, hail, animal strikes. |

| Is it mandatory? | Yes, in most states. | No, unless required by lender. |

| Deductible? | No (for others’ claims). | Yes, typically applies. |

Why You Need Both (Usually)

While liability is legally required in most places, comprehensive insurance often becomes a necessity, especially if you have a car loan or lease. Lenders typically insist on comprehensive (and collision) coverage to protect their investment in your vehicle.

Even without a loan, consider the financial hit of replacing your car after a fire or theft. For many, this would be a significant burden, making comprehensive coverage a worthwhile investment for peace of mind.

In my personal experience, opting for both has always provided a robust safety net. The small increase in premium can save you thousands if an unforeseen event damages your vehicle.

Factors to Consider When Choosing Coverage

Deciding on the right level of coverage involves weighing several personal factors. It’s not a one-size-fits-all decision; your choices should reflect your financial situation, vehicle value, and risk tolerance.

First, think about the value of your vehicle. If you drive an older car with low market value, paying for comprehensive coverage might not be financially sensible, as the premiums could quickly exceed the car’s worth over time.

- 💸 Car Value: High-value cars benefit more from comprehensive.

- 💰 Budget: Balance premiums with potential out-of-pocket costs.

- 🌍 Location: High theft rates or severe weather may warrant comprehensive.

- 📊 Risk Tolerance: How much financial risk are you comfortable taking?

- 🛣️ Driving Habits: Fewer miles might reduce your overall risk exposure.

The Importance of Your Deductible

Your deductible plays a significant role in how much you pay for comprehensive coverage. A higher deductible generally means lower premiums, but you’ll pay more out-of-pocket if you file a claim. Conversely, a lower deductible means higher premiums.

I always advise people to choose a deductible they can comfortably afford to pay at any given moment. Don’t set it so high that a claim would cause a financial crisis.

This is a balancing act between immediate savings on premiums and potential future costs. Carefully consider your emergency fund before making this decision.

When Can You Drop Comprehensive?

For many drivers, there comes a point when dropping comprehensive coverage makes financial sense. This usually happens when the annual premium cost approaches or exceeds a significant percentage of your car’s actual cash value (ACV).

If your car is only worth $2,000, and your comprehensive premium is $400 per year with a $500 deductible, you’re paying a substantial amount for diminishing returns. In such cases, self-insuring against non-collision damage might be a more economical choice.

Always do the math and compare the cost of coverage against your car’s current market value. Resources like Kelley Blue Book or Edmunds can help you determine your vehicle’s worth.

Building a Robust Auto Insurance Strategy

Ultimately, a smart auto insurance strategy involves more than just meeting minimums. It’s about protecting your assets, minimizing financial risk, and ensuring peace of mind, both for yourself and for others on the road.

Combining liability with comprehensive and collision coverage creates a full protection plan. Collision coverage, by the way, covers damage to your own vehicle if you hit another car or object. It’s the third leg of a common “full coverage” policy.

Don’t hesitate to shop around and compare quotes from different providers. Websites like NerdWallet or Bankrate can offer valuable insights and comparison tools. For broader financial news that can impact your decisions, check out Bloomberg.

Remember, your insurance needs can change over time. Regularly review your policy, especially after major life events like buying a new car, moving, or changing your financial situation.

In my experience, an annual review ensures you’re never over-insured or, more critically, under-insured. It’s a proactive step towards long-term financial security on the road.

Conclusion

Understanding the difference between liability and comprehensive auto insurance is fundamental to making informed decisions about your financial protection. Liability safeguards others from your actions, while comprehensive protects your own vehicle from a wide range of non-collision events. By carefully considering your vehicle’s value, your budget, and your risk tolerance, you can tailor an insurance policy that truly meets your needs.

What steps will you take today to review or update your current auto insurance coverage?