Creating a Debt Repayment Plan is a pivotal step towards achieving financial freedom. Indeed, for many beginner investors, navigating the complexities of personal debt can feel daunting. However, developing a clear strategy simplifies the process significantly. Specifically, two popular and effective methods, the Debt Snowball and the Debt Avalanche, offer structured approaches to conquer outstanding balances. This guide will explore both, helping you determine the best path for your unique financial situation.

Understanding Your Debt Landscape

Before diving into repayment strategies, comprehending your current debt is crucial. Therefore, gather all relevant information. This includes loan types, outstanding balances, interest rates, and minimum monthly payments. Common forms of debt include credit card balances, personal loans, student loans, and auto loans. Understanding these details empowers you to make informed decisions.

Interest rates, in particular, play a significant role. High-interest debts accumulate quickly, making them more expensive over time. Conversely, lower interest rates allow more of your payment to go towards the principal. Recognizing this distinction is fundamental for effective debt management. Ultimately, a clear picture of your obligations forms the foundation of any successful repayment plan.

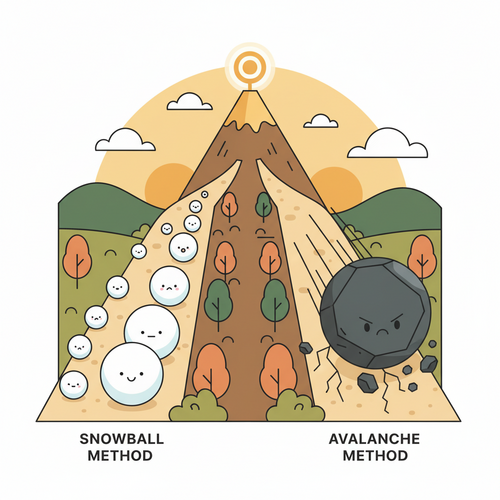

The Debt Snowball Method: Building Momentum

What is the Debt Snowball?

The Debt Snowball method prioritizes psychological wins over mathematical efficiency. Specifically, you focus on paying off your smallest debt first. Once that debt is eliminated, you roll the payment amount from the paid-off debt into the next smallest debt. This process creates a “snowball” effect, gaining momentum as each debt is cleared. Consequently, this method provides frequent motivation and a sense of progress.

How the Debt Snowball Method Works:

- List Your Debts: Organize all your debts from smallest balance to largest. Ignore interest rates for this initial step.

- Make Minimum Payments: Pay the minimum required amount on all debts except the smallest one.

- Attack the Smallest Debt: Devote all extra available funds to paying down the debt with the smallest outstanding balance.

- Roll Over Payments: Once the smallest debt is fully paid, take the money you were paying on it (minimum payment + extra funds) and add it to the minimum payment of the next smallest debt.

- Repeat the Process: Continue this cycle until all your debts are eliminated.

For instance, imagine having three debts: a $500 credit card, a $1,500 personal loan, and a $5,000 student loan. Using the snowball method, you would focus intensely on the $500 credit card. Once it is gone, the freed-up funds would then attack the $1,500 personal loan. This continuous process fuels motivation.

Pros and Cons of the Debt Snowball:

Indeed, a significant advantage of the snowball method is the psychological boost it provides. Eliminating debts quickly, even small ones, offers tangible proof of progress. This can be highly motivating, especially for individuals who might feel overwhelmed by their overall debt burden. Furthermore, these quick wins help maintain consistency and commitment to the plan. Consequently, adherence rates often remain high with this approach.

However, a drawback is that you might pay more interest over the long term. This occurs because the method doesn’t prioritize debts with higher interest rates. Therefore, while emotionally satisfying, it might not be the most financially efficient strategy. Individuals should weigh their need for motivation against potential extra interest costs. Ultimately, understanding this trade-off is vital.

The Debt Avalanche Method: Maximizing Savings

What is the Debt Avalanche?

Conversely, the Debt Avalanche method focuses on minimizing the total interest paid. This strategy prioritizes debts with the highest interest rates first. By tackling the most expensive debts initially, you save more money in the long run. Consequently, this method is often recommended for those seeking the most financially efficient path to debt freedom. It leverages mathematical logic over emotional satisfaction.

How the Debt Avalanche Method Works:

- List Your Debts: Organize all your debts from the highest interest rate to the lowest.

- Make Minimum Payments: Pay the minimum required amount on all debts except the one with the highest interest rate.

- Attack the Highest Interest Debt: Direct all extra available funds towards paying down the debt with the highest interest rate.

- Roll Over Payments: Once the highest interest debt is fully paid, take the money you were paying on it (minimum payment + extra funds) and add it to the minimum payment of the next debt with the highest interest rate.

- Repeat the Process: Continue this cycle until all your debts are eliminated.

For instance, consider the same three debts: a credit card with 22% APR, a personal loan with 10% APR, and a student loan with 5% APR. The avalanche method would instruct you to intensely focus on the credit card first, regardless of its balance. This strategic approach minimizes the total cost of borrowing. Investopedia offers further insights into financial concepts like these.

Pros and Cons of the Debt Avalanche:

Indeed, the primary benefit of the avalanche method is the significant savings on interest. By eliminating the most expensive debts first, you reduce the total amount you pay over the life of your loans. This makes it the mathematically superior choice for reducing overall debt cost. Furthermore, seeing the principal balance of high-interest debt decrease can be motivating for some individuals. It represents smart financial planning.

However, a potential downside is that it can feel slower initially. If your highest interest debt also has a large balance, it might take a considerable amount of time before you see it fully paid off. This lack of quick wins could be discouraging for some. Therefore, individuals must possess strong discipline and patience for this method to be effective. Forbes often discusses the importance of financial discipline.

Snowball vs. Avalanche: Which Method is Right for You?

Choosing between the Debt Snowball and Debt Avalanche methods depends largely on your personality and financial discipline. Both are effective in their own right. Specifically, the “best” method is the one you will stick with consistently. Therefore, self-awareness is key.

Consider the Debt Snowball if you:

- Need immediate motivation and quick wins to stay committed.

- Feel overwhelmed by your total debt and desire a psychological boost.

- Struggle with long-term financial discipline.

Conversely, consider the Debt Avalanche if you:

- Are highly disciplined and motivated by mathematical efficiency.

- Want to save the maximum amount of money on interest payments.

- Can remain patient even if initial progress feels slow.

Ultimately, assess your financial behavior and priorities. There is no one-size-fits-all answer. Your choice should align with what genuinely helps you stay on track. Both paths lead to debt freedom; they simply offer different journeys.

Creating Your Personalized Debt Repayment Plan

Regardless of the method you choose, a structured approach is essential. Therefore, begin by listing all your debts comprehensively. Include the creditor, current balance, interest rate, and minimum payment for each. This initial step provides clarity.

Next, create a detailed budget. Identify areas where you can cut expenses to free up extra money for debt payments. Even small adjustments can make a significant difference. Furthermore, consider increasing your income if possible. Every additional dollar directed towards debt accelerates your progress. The Wall Street Journal frequently features articles on budgeting and financial planning.

Once you have extra funds, apply your chosen method consistently. Stick to your plan, making extra payments diligently. Regularly review your progress. Adjust your budget as needed. Celebrate milestones, however small. This sustained effort will lead to success.

Beyond Repayment: Building a Strong Financial Future

Eliminating debt is a monumental achievement, but the journey doesn’t end there. Indeed, establishing sound financial habits is equally important. Therefore, prioritize building an emergency fund. This safety net protects you from unforeseen expenses, preventing new debt accumulation. Aim for three to six months of living expenses in an easily accessible savings account.

Furthermore, continue to live within your means. Avoid the temptation to take on new consumer debt. Focus on saving for future goals, such as retirement or a down payment on a home. Consider investing any additional funds. Bloomberg provides extensive resources on investment strategies. Continuously educate yourself about personal finance. CNBC is another excellent source for financial news and advice. Your disciplined approach to debt repayment can become a springboard for long-term wealth creation.

Conclusion

Creating a Debt Repayment Plan is a powerful declaration of financial independence. Whether you choose the motivating Debt Snowball or the financially optimized Debt Avalanche, the key lies in consistent action. Therefore, understand your debts, select a method that resonates with your personality, and commit to your plan. By taking control of your finances today, you pave the way for a more secure and prosperous tomorrow. Embark on this journey with confidence, knowing that every payment brings you closer to ultimate financial freedom.