Executive Summary

- Global fixed-income markets exhibit unprecedented volatility. Geopolitical shifts and macroeconomic policies are primary drivers.

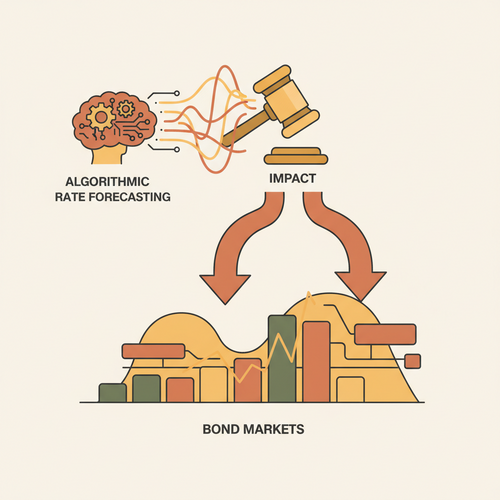

- Algorithmic rate forecasting leverages advanced machine learning. It provides critical predictive insights into yield curve dynamics.

- Integrating these models enhances risk management and portfolio optimization. Strategic asset allocation benefits significantly.

The Intricacies of Global Fixed-Income Volatility

Global fixed-income markets currently operate under extraordinary strain. Unprecedented volatility defines the current landscape. Geopolitical uncertainties contribute significantly to this instability. Central bank policy divergences exacerbate market movements. Inflationary pressures across major economies also play a pivotal role. These factors collectively create a challenging environment for traditional investment strategies.

Bond yields experience rapid and substantial fluctuations. This impacts sovereign debt, corporate bonds, and securitized products alike. Understanding these complex interdependencies is paramount. Traditional econometric models often struggle with non-linear relationships. They may fail to capture sudden regime shifts. Investors require more agile analytical tools.

Yield curve inversions signal potential economic downturns. Market participants closely monitor these indicators. Swift capital reallocation becomes essential. Hedging strategies must adapt quickly. This dynamic environment necessitates predictive capabilities beyond conventional methodologies.

Expert Insight: “The current macroeconomic paradigm demands a re-evaluation of fixed-income risk. Static duration management is no longer sufficient. Dynamic, model-driven approaches are imperative for capital preservation and alpha generation.”

Algorithmic Foundations in Interest Rate Forecasting

Algorithmic rate forecasting represents a significant evolution. It moves beyond subjective assessments. This methodology employs sophisticated computational techniques. It analyzes vast datasets to predict interest rate trajectories. Key inputs include macroeconomic indicators, market sentiment, and central bank communications. High-frequency trading data also informs these models.

The core principle involves identifying hidden patterns. These patterns drive future yield movements. Time-series analysis forms a foundational component. ARIMA and GARCH models provide baseline predictions. However, more advanced techniques offer superior accuracy. These include machine learning and artificial intelligence paradigms.

Model selection depends on specific forecasting horizons. Short-term predictions might favor deep learning. Long-term outlooks could utilize Bayesian methods. Feature engineering is critical for model performance. Relevant features include inflation expectations, unemployment rates, and global trade volumes. Data quality and integrity are non-negotiable for reliable outputs.

Machine Learning Paradigms for Yield Curve Prediction

Machine learning (ML) models offer distinct advantages. They excel at identifying non-linear relationships. Neural networks can process high-dimensional data. This makes them ideal for complex yield curve dynamics. Recurrent Neural Networks (RNNs) are particularly effective. They capture temporal dependencies in financial time series. Long Short-Term Memory (LSTM) networks mitigate vanishing gradient problems.

Ensemble methods further enhance predictive power. Random Forests and Gradient Boosting Machines combine multiple models. This reduces overfitting and improves generalization. Support Vector Machines (SVMs) are also deployed. They effectively classify market regimes. This assists in identifying periods of increased volatility or stability.

Validation techniques are crucial for robust model deployment. Cross-validation ensures model reliability. Out-of-sample testing provides realistic performance metrics. Backtesting simulates historical trading scenarios. This quantifies potential returns and risks. Model interpretability remains a challenge. Explainable AI (XAI) is gaining traction to address this.

- Key ML Models:

- LSTM Networks: Effective for time-series forecasting.

- Gradient Boosting Machines: Robust ensemble approach.

- Random Forests: Reduces variance, improves stability.

- Critical Considerations:

- Data stationarity and transformation.

- Hyperparameter tuning for optimal performance.

- Regularization techniques to prevent overfitting.

Quantifying Risk: Value at Risk and Stress Testing Methodologies

Effective risk management is paramount in volatile markets. Algorithmic rate forecasts feed directly into risk models. Value at Risk (VaR) is a standard metric. It quantifies potential losses over a specified period. Historical VaR, parametric VaR, and Monte Carlo VaR each offer unique insights. Value at Risk (VaR) provides a statistical estimate of maximum expected loss.

Stress testing complements VaR analysis. It evaluates portfolio performance under extreme scenarios. Hypothetical shocks include interest rate spikes or liquidity crises. Algorithmic models can simulate these conditions. They project how yield curves would react. This helps institutions prepare for Black Swan events. These simulations are critical for regulatory compliance.

Dynamic hedging strategies leverage these risk insights. Futures and options contracts are common instruments. Algorithms can identify optimal hedge ratios. This minimizes exposure to adverse rate movements. Portfolio duration management becomes more proactive. Convexity adjustments are also algorithmically determined. This optimizes bond portfolio sensitivity to interest rate changes.

Operationalizing Algorithmic Insights in Portfolio Management

Integrating algorithmic forecasts into daily operations is transformative. Portfolio managers gain a significant analytical edge. Real-time rate predictions inform asset allocation decisions. This enables timely adjustments to bond holdings. The objective is to optimize risk-adjusted returns consistently. This approach is distinct from passive index tracking.

Execution algorithms can automate trading strategies. They capitalize on minute market inefficiencies. Optimal execution pathways are identified. This minimizes market impact and transaction costs. The entire investment process becomes more systematic. Human biases are substantially reduced. This leads to more disciplined and objective decision-making.

Customizable dashboards provide actionable intelligence. Managers visualize yield curve shifts instantly. Model confidence levels are clearly displayed. Alerts trigger when market conditions deviate significantly. This ensures swift response to emerging opportunities or threats. Continuous model monitoring is also essential for performance. Calibration ensures forecasts remain relevant.

Regulatory Scrutiny and Ethical AI in Fixed-Income Markets

The increasing use of AI in finance attracts regulatory attention. Authorities focus on model transparency and fairness. Financial institutions must demonstrate model explainability. Bias in algorithms is a significant concern. Data inputs must be carefully vetted for embedded prejudices. Ethical AI frameworks are becoming industry standards.

Compliance with existing regulations is non-negotiable. MiFID II and Dodd-Frank govern trading practices. Algorithmic trading systems must adhere strictly to these rules. Audit trails are essential for accountability. Regulators scrutinize model risk management frameworks. Robust governance ensures model integrity and oversight.

The “black box” nature of some advanced AI models poses challenges. Explainable AI (XAI) addresses this directly. It aims to make model decisions interpretable. This builds trust among stakeholders. Financial firms invest heavily in XAI research. Transparent algorithms foster market stability and investor confidence. Understanding the Yield Curve is fundamental to these discussions.

Future Trajectories: Quantum Computing and Advanced Neural Networks

The horizon for algorithmic rate forecasting is expanding rapidly. Quantum computing holds immense promise. It could revolutionize computational finance. Solving complex optimization problems will become faster. Simulating intricate market dynamics will be more precise. Quantum machine learning algorithms are in early development stages.

Advanced neural network architectures are also emerging. Graph Neural Networks (GNNs) can model complex relationships. They analyze networks of financial instruments effectively. Generative Adversarial Networks (GANs) create synthetic data. This enhances model training in data-scarce environments. These innovations will further refine predictive accuracy.

Hybrid models, combining traditional finance with AI, will proliferate. Explainable AI will become increasingly sophisticated. Regulatory frameworks will evolve to encompass new technologies. The drive for higher alpha and robust risk management will persist. Continuous innovation remains key to competitive advantage in fixed-income markets.

Conclusion

Global fixed-income volatility presents persistent challenges. Algorithmic rate forecasting offers a powerful countermeasure. It provides clarity through complex market dynamics. Advanced machine learning models enhance predictive accuracy. Robust risk management frameworks are intrinsically linked.

Operationalizing these insights drives superior portfolio performance. Ethical considerations and regulatory compliance are paramount. The future promises even more sophisticated tools. Continuous adaptation is essential for market participants. Are you leveraging cutting-edge algorithmic intelligence to navigate fixed-income markets effectively?