Introduction

Many of us pay for various types of insurance every month. It is a regular and necessary part of our budget. For example, we pay for our car, our home, or our health coverage. But have you ever stopped to wonder how the business of insurance actually works? How can these companies take in relatively small monthly payments? And how can they then afford to pay for huge, unpredictable claims, like a totaled car or a major surgery?

The business model of an insurance company is a fascinating blend of risk management and investing. It is not as simple as just collecting more money than they pay out. Understanding this model can help you become a more informed consumer. This guide will pull back the curtain. We will explain in simple terms the two main ways that insurance companies make money.

The Two Engines of Profit

First, it is important to understand that an insurance company’s profitability is driven by two primary engines. Both of these engines must be running well for the company to be successful and stable.

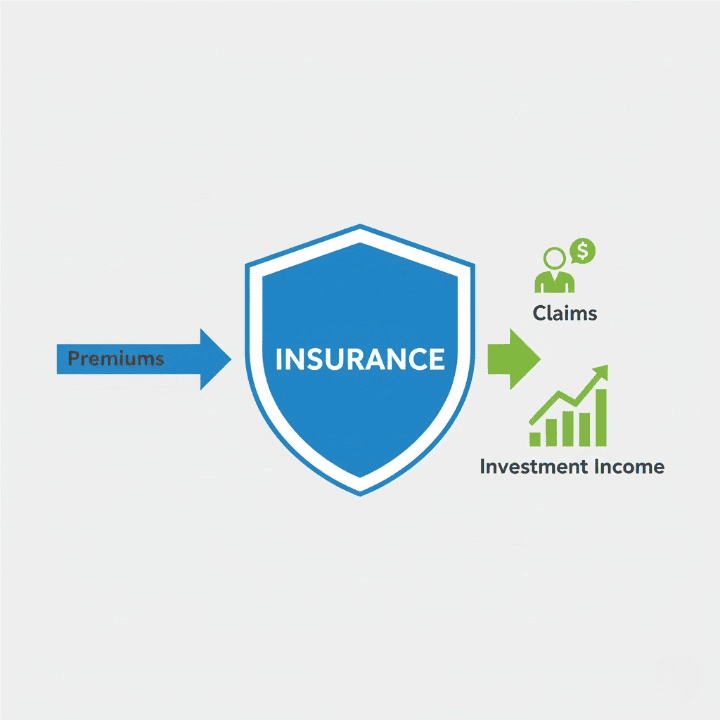

Engine 1: Underwriting Profit. This is the money that the company makes directly from its core business of selling insurance policies.

Engine 2: Investment Income. This is the money that the company makes by investing the premiums it collects from all of its policyholders.

A financially healthy insurance company aims to be profitable in both areas. However, as we will see, the investment income is often so powerful that it can make up for losses in the underwriting department. Let’s break down each of these engines in more detail.

Engine 1: The Math of Underwriting

The first engine, underwriting, is the process of evaluating risk. Insurers use this process to decide who to insure and what price, or “premium,” to charge for that coverage. The goal of underwriting is straightforward. The company wants to collect more money in premiums than it pays out in claims and other operating expenses.

The Law of Large Numbers

This entire process is built on a key statistical concept. This concept is the “law of large numbers.” An insurance company cannot predict which specific individual will have a car accident next year. However, by insuring a very large group of people, like millions of drivers, they can use historical data to very accurately predict how many accidents will occur within that entire group. This allows them to calculate the total amount they will likely need to pay in claims.

Risk Assessment and Your Premium

Next, the company must assess the risk of each individual applicant. This is how they determine your personal premium. They use a wide range of data points to predict your likelihood of filing a claim. For example, for auto insurance, they will look at your driving record, your age, and the type of car you drive. For health insurance, they will look at your age and medical history.

In many places, they will also use a credit-based insurance score. This score is derived from your credit report. Statistics have shown a correlation between how a person manages their credit and their likelihood of filing a claim. This is a key reason why good financial management can sometimes lead to lower insurance costs.

After assessing your risk, they will place you in a “risk pool” with other people who have a similar profile. The premium for that pool is calculated to be enough to cover the predicted claims for the group, plus the company’s operating expenses and a margin for profit. The simple formula for underwriting profit is: Premiums Collected – (Claims Paid + Operating Expenses) = Underwriting Profit

Engine 2: The Power of the Investment “Float”

The second engine of profit is often more powerful and less understood by the public. This is the income that insurance companies generate from their investments.

Think about it this way. You and millions of other people pay your insurance premiums every month. However, you do not file a claim every month. This creates a massive pool of money that the insurance company holds. This pool of money is called the “float.” It is made up of all the premiums that have been collected but have not yet been paid out in claims.

Insurance companies do not just let this massive float of cash sit in a bank account. Instead, they invest it. They typically put this money into a diverse portfolio of relatively safe and stable assets. This most commonly includes government and corporate bonds.

The income they generate from these investments is a huge source of profit for them. The returns they get are heavily dependent on the overall interest rate environment in the economy. When the general interest rate is high, they earn more on their bond portfolio.

This investment income is so significant that some insurance companies can actually operate at a small underwriting loss and still be very profitable overall. They might pay out slightly more in claims and expenses than they collect in premiums. However, they can make up for this loss and much more through the returns they earn on their float.

Why This Business Model Matters to You

Understanding this business model helps you, the consumer, make sense of your own insurance experience. It explains why certain things are the way they are.

For example, you can now understand why your personal data, like your driving history or your credit, is so important to the insurer. It is a key part of their underwriting calculations. You can also understand why they investigate claims carefully. They must manage claims payouts to maintain their underwriting profitability and to protect the entire pool from fraud.

This knowledge helps you see insurance as a business transaction. In exchange for your premium, the company is providing a form of financing for your potential future losses. You often use your credit card to pay for this service. This creates a more balanced and informed relationship between you and your provider.

Conclusion

In summary, insurance companies make money in two primary ways. The first is through underwriting profit, which is the money they aim to make from the premiums you pay. The second, and often more powerful, way is through the investment income they earn on the massive pool of premiums they hold, known as the float.

This business model is a constant balancing act between assessing risk and managing investments. By understanding how this industry works from the inside, you become a more informed and empowered consumer. You can better appreciate the value that your insurance policy provides. You can also understand the factors that go into the prices you are charged. This knowledge is a key part of smart and comprehensive financial management.