Introduction

You have likely noticed it in your daily life. The price of groceries, gasoline, and other essential goods seems to go up over time. This phenomenon is called inflation. Around the same time you start hearing news reports about rising inflation, you often hear another piece of news. This is about the nation’s central bank deciding to raise the interest rate. This is not a coincidence.

In fact, this is a deliberate and powerful cause-and-effect relationship that forms the bedrock of modern economic policy. Understanding the connection between inflation and interest rates is a key piece of financial literacy. It helps you understand the world around you. This guide will explain this powerful connection in simple terms. We will show you why it happens and what it means for your personal finances.

What is Inflation? The Erosion of Purchasing Power

First, let’s define inflation simply. Inflation is the rate at which the general level of prices for goods and services is rising. Consequently, the purchasing power of your money is falling.

Let’s use a clear example. A cup of coffee that cost you $3.00 last year might cost you $3.20 this year. That 20-cent increase is a direct reflection of inflation. The coffee itself did not change, but the value of each dollar you hold has slightly decreased.

A small amount of inflation, typically around 2%, is considered normal and is often a sign of a healthy, growing economy. However, when inflation becomes too high, it becomes a problem. High inflation erodes the value of your savings. It also makes it harder for families to afford everyday necessities. This is when a nation’s central bank must step in.

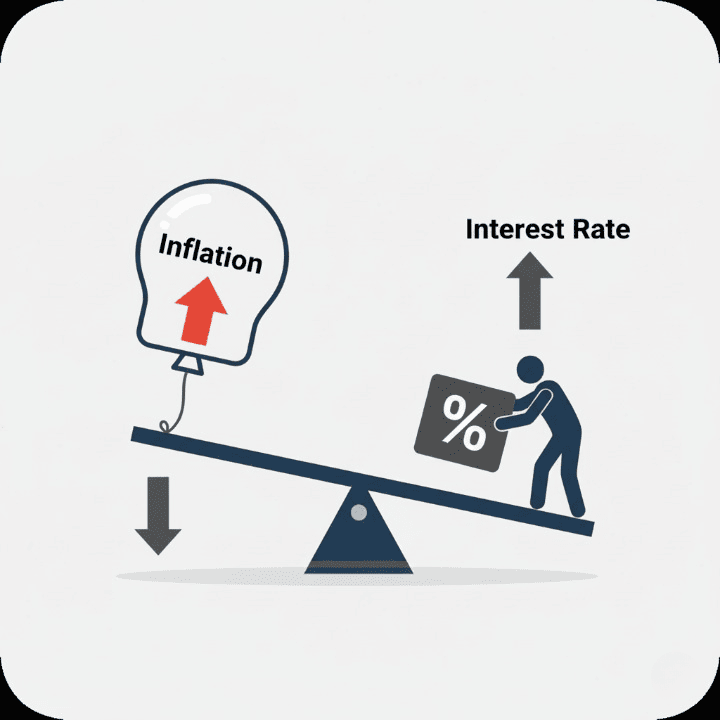

The Central Bank’s Role: Fighting Inflation with Interest Rates

The primary job of a nation’s central bank, such as the U.S. Federal Reserve, is to maintain price stability. In other words, its main goal is to control inflation. The most powerful tool it has to accomplish this is its ability to set the key interest rate for the economy.

The “Why”: The Need to Cool Down the Economy

High inflation is often a symptom of an “overheating” economy. This means there is too much money chasing too few goods and services. When demand outpaces supply, prices are naturally pushed higher. To bring prices back under control, the central bank needs to “cool down” the economy. It needs to reduce the overall demand for goods and services.

The “How”: Making Borrowing More Expensive

The central bank achieves this by raising its key interest rate. This is the rate at which commercial banks borrow money from each other. When this baseline rate goes up, commercial banks, in turn, pass this higher cost on to their customers. This results in a higher interest rate on all new financing in the economy. Mortgages, auto loans, and business loans all become more expensive. The goal is to make borrowing and spending less attractive for both consumers and businesses.

The Direct Impact on Your Personal Finances

This macroeconomic action has a very direct and personal impact on your wallet. Here is how it typically affects you.

1. The Cost of New Borrowing Rises. First, the most immediate effect is that any new financing becomes more expensive. If you are planning to get a mortgage for a home or a loan for a car, you will be offered a higher interest rate than you would have been a few months earlier. This is the central bank’s strategy in action. The higher cost is meant to discourage you from making that large purchase, thereby reducing overall demand in the economy.

2. Your Credit Card Debt Becomes More Expensive. Next, most credit card agreements have a variable interest rate. This rate is usually tied to a benchmark known as the prime rate. The prime rate moves in lockstep with the central bank’s key rate. Therefore, when the central bank announces a rate hike, the APR on your credit card balance will also go up automatically, usually within one or two billing cycles.

3. Saving Finally Becomes More Rewarding. There is, however, a silver lining for savers. In an effort to attract more deposits, banks will also raise the interest rate they offer on savings products. High-yield savings accounts and Certificates of Deposit (CDs) will begin to pay a much more meaningful return. This rewards people for saving money instead of spending it.

4. The Broader Economy May Slow Down. Finally, the intended overall effect is to reduce demand across the entire economy. This can sometimes mean a slowdown in the job market as businesses pull back on expansion plans. This is a key reason why central banks try to act carefully. They want to control inflation without causing a major economic downturn.

How to Manage Your Finances in a High-Inflation Environment

When you know that inflation is high and interest rates are rising, you can take a few smart steps to protect your financial health.

First, you should make it your top priority to pay down any high-interest, variable-rate debt. This especially means your credit card balances, as their cost is actively increasing.

Next, you must review your budget carefully. With the prices of everyday goods on the rise, you may need to adjust your spending habits to stay on track with your long-term goals.

You should also take advantage of the higher rates on savings. This is a great time to shop around for a high-yield savings account to make sure your cash is working as hard as possible for you.

Finally, you need to protect your credit. Making all of your payments on time and managing your debt wisely is even more crucial during these times. A strong credit profile will help you qualify for the best available rates if you do end up needing a loan. Having good insurance coverage is also key, as an unexpected loss can be even more devastating when prices are high.

Conclusion

In conclusion, the relationship between inflation and the interest rate is one of the most fundamental concepts in financial management. It is a direct cause-and-effect loop that has a major impact on our financial lives.

We have seen that high inflation causes the central bank to raise the interest rate. The bank does this to cool down the economy and stabilize prices. This action, in turn, makes borrowing more expensive and saving more rewarding for you as a consumer.

By understanding this important connection, you are no longer just a passive observer of economic news. You can understand the “why” behind the headlines. This knowledge empowers you to make smarter financial decisions. Ultimately, it helps you to protect and improve your financial health, no matter what the economic climate looks like.