Executive Summary

- Systemic risk securitization transforms unquantifiable financial contagion into tradable instruments.

- Advanced reinsurance protocols leverage capital markets, enhancing global financial stability and risk diversification.

- Operationalizing these strategies demands sophisticated analytics, robust regulatory compliance, and continuous innovation.

The financial landscape constantly evolves. New challenges necessitate sophisticated risk mitigation strategies. Understanding systemic risk securitization and advanced reinsurance protocols is now paramount for market participants.

These mechanisms offer critical tools. They manage complex interdependencies within global financial systems. Their proper implementation supports market resilience and investor confidence.

Deconstructing Systemic Risk Vulnerabilities

Systemic risk represents the potential for an entire financial system to collapse. This occurs due to interconnectedness. A failure in one institution or market segment can trigger a cascade across others.

The 2008 global financial crisis highlighted these vulnerabilities. It exposed the limitations of traditional risk management. Identifying and quantifying these interdependencies remains a core challenge.

Macroprudential supervision aims to monitor system-wide risks. It implements policies to mitigate contagion. However, inherent market complexities often exceed conventional oversight capacities.

Understanding tail risk events is crucial. These low-probability, high-impact scenarios drive systemic instability. Effective protocols must address these extreme outcomes proactively.

The Architecture of Risk Securitization Instruments

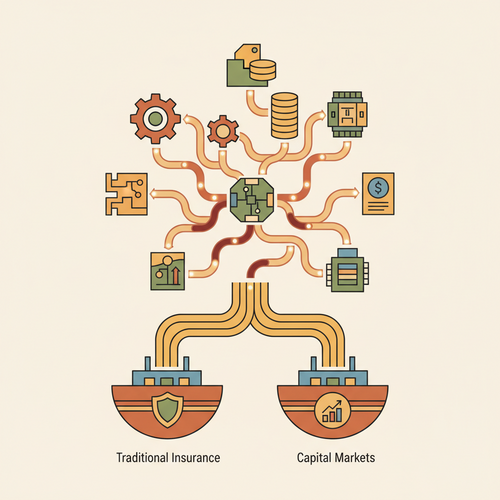

Risk securitization transforms illiquid assets or risk exposures into tradable securities. This process transfers risk from originators to capital market investors. It enhances liquidity and capital efficiency.

Special Purpose Vehicles (SPVs) are central to this architecture. They isolate the underlying risks. This structure insulates investors from the originator’s credit risk, known as bankruptcy remoteness.

Catastrophe bonds (Cat Bonds) exemplify this innovation. They offer high yields to investors. In return, investors assume specific peril risks, like hurricanes or earthquakes.

Insurance-Linked Securities (ILS) represent a broader category. This includes mortality bonds and weather derivatives. These instruments diversify investor portfolios, offering uncorrelated returns.

Securitization creates tranches with varying risk-return profiles. Senior tranches carry lower risk and yield. Junior tranches offer higher returns but assume greater risk exposure. Securitization fundamentally reallocates risk.

Expert Insight: “Effective securitization demands rigorous actuarial modeling. It requires transparent disclosure of underlying risk parameters. Investor confidence hinges on this clarity.”

Innovations in Advanced Reinsurance Protocol Design

Reinsurance traditionally provides capital relief to primary insurers. Advanced protocols move beyond simple retrocession. They integrate sophisticated risk transfer mechanisms and capital market solutions.

Parametric triggers are a key innovation. Payouts are based on predefined indices, not actual losses. Examples include wind speed or earthquake magnitude. This eliminates basis risk for the reinsurer.

Indemnity-based solutions remain vital. However, parametric designs offer speed and transparency. They reduce claims adjustment costs and accelerate post-event liquidity for insurers.

Contingent capital facilities provide pre-arranged funding. They activate upon specified loss events. This ensures capital availability precisely when needed, stabilizing insurer solvency.

Sidecar arrangements create temporary SPVs. These co-participate in specific reinsurance programs. They allow institutional investors direct access to underwriting profits, enhancing capital deployment flexibility.

Dynamic financial analysis (DFA) underpins these designs. It uses stochastic modeling to project financial outcomes. This optimizes capital allocation and reinsurance purchasing decisions.

Capital Market Integration: Bridging Risk and Liquidity

The integration of capital markets into reinsurance profoundly alters risk transfer. It expands the capacity for managing mega-catastrophes. Traditional balance sheets alone cannot absorb such shocks.

Institutional investors seek uncorrelated assets. ILS offer attractive returns independent of broader economic cycles. This creates a powerful synergy between insurance needs and investment goals.

This convergence enhances capital efficiency for insurers. It reduces reliance on traditional equity or debt financing for peak risks. This frees up capital for core underwriting activities.

Regulatory arbitrage is a potential consideration. Structuring risks through capital markets may face different capital requirements. Jurisdictional variances can influence structuring decisions.

The liquidity transformation is significant. Illiquid insurance risks become highly tradable securities. This benefits both originators seeking capital and investors seeking yield and diversification.

Regulatory Frameworks and Compliance Imperatives

Navigating the regulatory landscape for systemic risk securitization is complex. Regulators prioritize financial stability and consumer protection. Strict compliance is non-negotiable.

Solvency II in Europe mandates robust risk management and capital adequacy. It influences how insurers structure and collateralize reinsurance agreements. Transparency requirements are stringent.

Basel III for banks also impacts financial institutions involved. It governs capital requirements and liquidity ratios. Interconnectedness between banking and insurance sectors necessitates coordinated oversight.

Risk-Based Capital (RBC) standards vary by jurisdiction. These determine the capital held against various risk exposures. Securitized risks must align with these frameworks.

Disclosure requirements are paramount. Investors need comprehensive information on underlying risks. Rating agencies play a vital role in assessing instrument creditworthiness.

Market Warning: “Inadequate regulatory oversight or inconsistent jurisdictional standards could inadvertently introduce new forms of systemic risk. Harmonization efforts are critical.”

Operationalizing Advanced Reinsurance Solutions

Implementing advanced reinsurance protocols requires sophisticated operational capabilities. It moves beyond traditional manual processes. Technology and data analytics are foundational.

Exposure modeling is an essential first step. High-resolution data and geospatial analytics pinpoint vulnerable assets. This informs pricing and structuring decisions for securitized risks.

Underwriting complex securitized deals demands specialized expertise. Actuaries, quants, and legal professionals collaborate. They assess intricate risk layers and contractual obligations.

Post-event claims processing must be efficient. For parametric triggers, automated systems can accelerate payouts. Indemnity-based structures require robust loss verification protocols.

Emerging technologies offer new frontiers. Blockchain can enhance transparency and contract execution. Artificial intelligence and machine learning improve predictive modeling and fraud detection.

Continuous monitoring of portfolio performance is crucial. Stress testing against various scenarios ensures ongoing capital adequacy. This proactive approach sustains market confidence. Systemic risk remains a constant challenge.

Future Trajectories in Risk Transfer Evolution

The landscape of risk transfer is dynamic. New perils and evolving exposures drive innovation. The convergence of traditional and alternative capital will only intensify.

Climate risk securitization is gaining prominence. Instruments tailored for extreme weather events will become more commonplace. This addresses growing environmental vulnerabilities.

Cyber risk poses a unique challenge. Its intangible nature and aggregation potential are significant. Securitization structures are being explored for this complex and emerging threat.

Greater transparency and standardization are likely. This will enhance market liquidity and investor participation. Common reporting frameworks could emerge across jurisdictions.

The role of data will expand exponentially. Advanced analytics will unlock deeper insights into risk correlations. This allows for more precise pricing and more efficient capital deployment.

Adaptive strategies will be key. Financial institutions must continually refine their risk transfer frameworks. This ensures resilience against unforeseen market shocks and evolving systemic threats.

Conclusion

Systemic risk securitization and advanced reinsurance protocols are indispensable. They fortify the global financial architecture. These instruments redistribute complex exposures efficiently.

Their successful implementation hinges on expertise. It demands technological integration and robust regulatory oversight. The financial system gains stability and enhanced capacity.

As markets evolve, so too must risk management. Continuous innovation is essential. Are your risk transfer strategies optimally positioned for future systemic challenges and opportunities?