Introduction

Navigating the world of life insurance can feel complex, especially when you are trying to understand how these policies might contribute to your broader financial strategy. Many people view life insurance primarily as a safety net, a way to protect loved ones financially after an unexpected event. However, some types of life insurance also offer features that can potentially help build wealth over time.

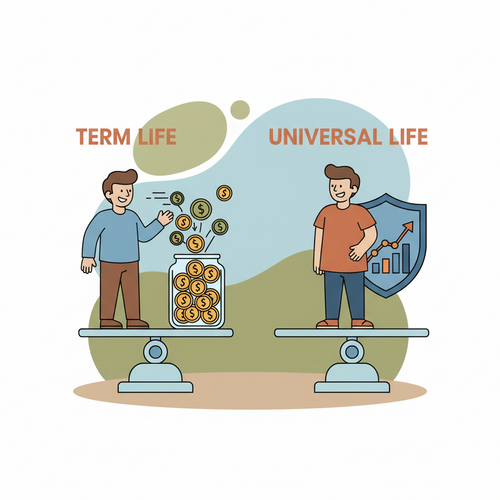

This raises a crucial question for many investors and financial planners: when comparing Term Life vs Universal Life Insurance, which policy truly builds more wealth? The answer is not always straightforward. It depends heavily on your individual financial goals, risk tolerance, and how you manage your overall investments.

Understanding the fundamental differences between these two popular insurance options is essential. We will explore their structures, benefits, and how each might fit into a comprehensive wealth-building plan. Our goal is to equip you with the knowledge to make informed decisions about your financial future.

Understanding Term Life Insurance

What is Term Life Insurance?

Term life insurance is perhaps the simplest and most direct form of life insurance. It provides coverage for a specific period, or “term,” such as 10, 20, or 30 years. If the insured person passes away during this term, the policy pays a death benefit to the designated beneficiaries. However, if the term expires and the insured is still living, the coverage typically ends, and there is no payout.

Crucially, term life insurance does not accumulate any cash value. This means it functions purely as protection. Think of it like renting an apartment; you pay for the use of the space for a period, but you do not build equity. Because of this straightforward nature and lack of a savings component, term life policies generally have significantly lower premiums compared to permanent life insurance options.

How Term Life “Builds” Wealth (Indirectly)

While term life insurance does not build cash value directly, it can play a vital role in your wealth-building strategy. Its primary function is to provide essential financial protection. This protection is invaluable for individuals with dependents or significant financial obligations, such as a mortgage or outstanding debts.

By securing a death benefit, term life insurance ensures that your loved ones will have financial support if you are no longer there to provide for them. This peace of mind allows you to focus your financial resources on other wealth-building vehicles. For example, the lower premiums of a term policy free up more of your disposable income. This freed-up capital can then be invested into assets with higher growth potential.

Many financial advisors advocate for the “buy term and invest the difference” strategy. This approach suggests purchasing an affordable term life policy for protection and then actively investing the money saved on premiums into a diversified portfolio. This could include stocks, bonds, mutual funds, or real estate. Over the long term, these external investments often yield higher returns than the cash value component of permanent life insurance policies. This strategy effectively leverages the protective aspect of term life while maximizing investment growth potential elsewhere.

Exploring Universal Life Insurance

What is Universal Life Insurance?

Universal life (UL) insurance is a type of permanent life insurance. Unlike term life, it is designed to last for your entire life, provided premiums are paid. A key feature of UL policies is their flexibility. Policyholders can often adjust their premium payments and even their death benefit amounts within certain limits, making it adaptable to changing financial circumstances.

Beyond the death benefit, universal life insurance includes a savings or investment component known as cash value. A portion of each premium payment, after expenses and the cost of insurance, is allocated to this cash value account. This cash value grows over time on a tax-deferred basis, which can be an attractive feature for long-term financial planning.

How Universal Life Builds Cash Value

The cash value component is where universal life insurance truly differentiates itself. It grows based on an interest rate credited to the account. However, the mechanism of this interest crediting can vary significantly among different types of universal life policies:

- Traditional Universal Life: The cash value earns a minimum guaranteed interest rate, along with potential additional interest based on the insurer’s performance.

- Indexed Universal Life (IUL): The cash value growth is linked to the performance of a specific stock market index, like the S&P 500, but with caps on potential gains and floors on potential losses.

- Variable Universal Life (VUL): Policyholders can direct their cash value into various investment sub-accounts, similar to mutual funds. This offers potentially higher returns but also carries market risk, meaning the cash value can decrease if investments perform poorly.

The cash value in a universal life policy offers a unique advantage: it can be accessed during the policyholder’s lifetime. You can take out loans against the cash value or make withdrawals. Loans are typically not taxable, and withdrawals are tax-free up to the amount of premiums paid. However, accessing the cash value can reduce the death benefit and may lead to surrender charges if the policy is terminated early. Understanding these mechanics is crucial for assessing its wealth-building potential.

For more details on how permanent life insurance policies accumulate cash value, you can refer to resources from reputable financial institutions. For instance, Investopedia provides comprehensive guides on various life insurance types and their cash value components: Cash Value Life Insurance Explained.

Key Differences and Wealth Building Potential

Cost and Flexibility

The differences in cost and flexibility are central to understanding which policy might better serve your wealth-building objectives. Term life insurance is almost always more affordable initially. Its premiums are fixed for the chosen term and are significantly lower than those for a comparable universal life policy.

This affordability makes term life accessible to more people. It ensures essential protection without demanding a large portion of your income. However, upon renewal at the end of the term, premiums can increase substantially, especially as you age. Term life offers very little flexibility beyond choosing the initial term and death benefit.

Conversely, universal life insurance comes with higher premiums, reflecting its permanent coverage and cash value component. However, it offers considerable flexibility. Policyholders can often adjust premium payments. If the cash value has grown sufficiently, you might even be able to pay premiums using the cash value itself for a period. You can also adjust the death benefit, increasing or decreasing it as your needs change (subject to underwriting and policy limits).

Cash Value Growth and Investment

When considering wealth building, the growth of the cash value is a major point of comparison. With universal life, the cash value grows on a tax-deferred basis. This means you do not pay taxes on the investment gains until you withdraw them. This deferred growth can be advantageous, especially over long periods.

However, it is important to understand the actual rate of return. The growth rate credited to UL policies often lags behind what one might achieve by investing directly in the market. Furthermore, various fees and charges, including administrative costs, mortality charges, and surrender charges, are deducted from the cash value. These fees can significantly impact the net growth, potentially making the internal rate of return lower than expected. For example, a study from the National Association of Insurance Commissioners (NAIC) could provide insights into industry-wide fee structures.

With term life insurance, since there is no cash value, the “wealth building” comes from the money you save on premiums. This savings can be invested independently. By doing so, you have complete control over your investment choices and can pursue potentially higher returns, albeit with corresponding market risks. Historically, well-diversified stock market investments have offered higher average annual returns than the guaranteed or typical returns seen in traditional universal life cash value accounts.

Risk and Control

The level of risk and control also differs significantly. Term life insurance carries minimal investment risk for the policyholder. Its purpose is pure protection. Your main concern is whether you will outlive the term, in which case the coverage ends.

Universal life insurance introduces varying degrees of investment risk. Traditional UL policies typically offer more stable, though often lower, returns. However, indexed universal life (IUL) and variable universal life (VUL) policies expose you to market fluctuations. With VUL, if your chosen sub-accounts perform poorly, your cash value can decrease. This can even lead to the need for higher premium payments to maintain coverage.

Furthermore, with term life and external investments, you maintain full control over your investment portfolio. You decide where to allocate your funds, how much risk to take, and when to buy or sell assets. With universal life, while you might have some choices in VUL sub-accounts, the overall structure and fees are determined by the insurance company. This means less direct control over the investment component compared to managing your own brokerage account.

It’s crucial to consider these risk and control factors when evaluating which policy aligns better with your wealth accumulation strategy. For insights into managing investment risk, resources from the Securities and Exchange Commission (SEC) are invaluable: Investing basics from the SEC.

Choosing the Right Policy for Your Financial Goals

When Term Life Might Be Better

Term life insurance often makes sense for several financial situations. First, it is ideal for individuals or families working with a tighter budget. The lower premiums allow them to secure substantial coverage without undue financial strain. This is particularly important during periods of high financial responsibility, such as raising young children or paying off a mortgage.

Second, term life is a strong choice for those who prefer to manage their investments independently. If you are comfortable and disciplined in investing your savings into stocks, bonds, or other growth-oriented assets, the “buy term and invest the difference” strategy can potentially lead to greater wealth accumulation over time. You gain direct control and the opportunity for higher market returns.

Finally, if you have a clear end date for your financial obligations—for instance, when your children become independent or your mortgage is paid off—a term policy can align perfectly. It provides robust coverage for that specific critical period, after which your need for extensive life insurance might diminish.

When Universal Life Might Be Better

Universal life insurance, despite its higher cost, serves distinct financial objectives. It is often considered by individuals looking for permanent life insurance coverage. This is especially true for long-term estate planning or for those who wish to leave a legacy, ensuring a death benefit will always be available.

Furthermore, UL policies appeal to those who desire a savings or investment component integrated directly within their insurance. The tax-deferred cash value growth can be a powerful tool, particularly for high-net-worth individuals seeking additional avenues for tax-advantaged savings beyond traditional retirement accounts. The ability to access cash value through loans or withdrawals can also provide a flexible source of funds in retirement or for emergencies, without immediately triggering taxable events.

The flexibility in premium payments and death benefit adjustments also makes universal life attractive to individuals whose financial situations might fluctuate over their lifetime. It provides a degree of adaptability that term policies simply do not offer. This makes it a suitable option for those who value comprehensive, lifelong coverage with an embedded savings feature.

Conclusion

Ultimately, the choice between Term Life vs Universal Life Insurance for building wealth boils down to individual priorities and financial philosophy. Term life insurance offers straightforward, affordable protection. It allows you to maximize your external investment opportunities due to its lower cost. Its indirect approach to wealth building relies on your discipline to invest the premium savings effectively, potentially leading to higher overall returns.

Universal life insurance, on the other hand, provides permanent coverage with a built-in cash value component that grows on a tax-deferred basis. While its internal returns might be modest compared to aggressive market investments, it offers flexibility and a unique tax-advantaged savings vehicle. It can be particularly attractive for long-term estate planning and for those who appreciate the convenience of an integrated insurance and savings product.

There is no single “better” policy; rather, there is a policy that is better suited to your specific circumstances. Consider your budget, your investment savvy, your need for lifelong coverage, and your tolerance for risk. Before making a final decision, it is always wise to consult with a qualified financial advisor. They can help you assess your needs, compare policy options, and integrate life insurance seamlessly into your broader financial plan.