Understanding the fundamental bond prices and interest rates relationship is crucial for any beginner investor. Indeed, these two financial concepts are intricately linked, often moving in opposite directions. Therefore, grasping this connection helps you make smarter investment decisions. This article will demystify this inverse relationship, explaining why it matters to your portfolio.

What Exactly Are Bonds?

First, let us define what a bond is. Essentially, a bond represents a loan. When you buy a bond, you are lending money to an entity, such as a government or a corporation. Furthermore, this entity promises to pay you back your principal amount on a specific date, known as the maturity date. In addition, they typically pay you regular interest payments along the way.

Key Bond Terms to Know

- Face Value (Par Value): This is the initial amount the bond issuer borrows. Consequently, it is also the amount they will repay you at maturity, assuming no default.

- Coupon Rate: Specifically, this is the fixed annual interest rate the bond issuer pays to you. It is expressed as a percentage of the face value.

- Maturity Date: This is the date when the bond expires. By this date, the issuer must return your face value.

- Yield: Yield represents the total return an investor receives from a bond. It considers the coupon payments and any capital gains or losses.

For instance, imagine a company issues a bond with a $1,000 face value and a 5% coupon rate. This means they will pay you $50 in interest per year. Subsequently, at maturity, they will repay your initial $1,000. Therefore, bonds provide a predictable income stream.

Understanding Interest Rates

Interest rates are simply the cost of borrowing money. They represent the fee a borrower pays to a lender for the use of assets. Conversely, they also represent the return a lender earns on an investment. Various factors influence interest rates, including economic growth and inflation.

Who Influences Interest Rates?

Central banks, like the U.S. Federal Reserve, play a significant role in setting interest rates. Specifically, they use monetary policy tools to influence the economy. When the economy needs stimulating, central banks might lower rates. Consequently, borrowing becomes cheaper, encouraging spending and investment.

However, if inflation is a concern, central banks might raise interest rates. This makes borrowing more expensive. Furthermore, it slows down economic activity to cool inflation. Therefore, central bank decisions ripple through financial markets, impacting everything from mortgages to bond prices.

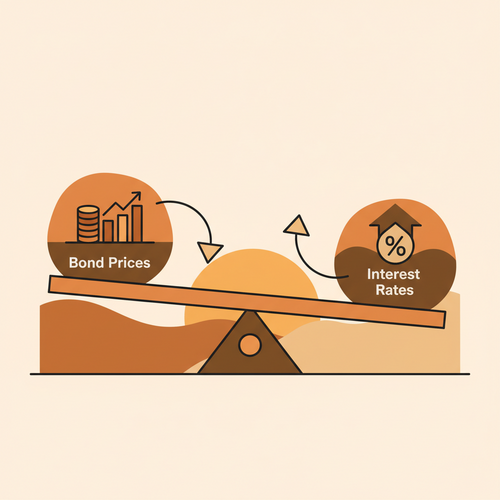

The Inverse Relationship Between Bond Prices and Interest Rates Explained

Now, let’s dive into the core concept: the inverse bond prices and interest rates relationship. When prevailing interest rates rise, the price of existing bonds generally falls. Conversely, when interest rates fall, the price of existing bonds tends to rise. This might seem counterintuitive at first glance, but it makes perfect sense with a little explanation.

Why Do They Move Oppositely?

Consider a bond you already own. Let us say it has a 3% coupon rate. This means it pays 3% interest on its face value annually. Now, imagine new bonds are being issued in the market with a 5% coupon rate. These new bonds offer a higher return to investors. Consequently, your older 3% bond becomes less attractive.

To make your older 3% bond competitive with the new 5% bonds, its market price must drop. Indeed, this price reduction makes its effective yield (yield-to-maturity) more comparable to the higher rates available. Therefore, investors will only buy your 3% bond at a discount. Conversely, if new bonds offer only 1% interest, your 3% bond becomes highly desirable, increasing its market price.

Example: Rising Interest Rates

Suppose you bought a brand new bond one year ago for $1,000. It pays a fixed 3% annual interest, meaning you get $30 a year. Now, however, the central bank raises interest rates. Consequently, newly issued bonds start offering a 5% coupon rate. Your existing 3% bond is suddenly less appealing.

If you wanted to sell your 3% bond today, prospective buyers would compare it to the new 5% bonds. They would not pay $1,000 for a bond paying $30 when they could buy a new bond for $1,000 paying $50. Therefore, to attract buyers, you would need to sell your 3% bond for less than $1,000. This is the essence of why bond prices fall when interest rates rise.

Example: Falling Interest Rates

Conversely, let us consider a scenario where interest rates fall. You own a bond purchased for $1,000, paying a 5% annual coupon. This provides you with $50 per year. Suppose the central bank then lowers interest rates significantly. Subsequently, newly issued bonds now only offer a 2% coupon rate.

Your existing 5% bond suddenly looks very attractive to investors. Indeed, it offers a much higher annual payment than newly issued bonds. Consequently, if you decided to sell your bond, buyers would be willing to pay more than $1,000 for it. This premium reflects the higher interest payments your bond provides compared to current market rates. Thus, bond prices rise when interest rates fall.

Factors Influencing Bond Prices Beyond Interest Rates

While interest rates are a primary driver, other factors also impact bond prices. Understanding these elements provides a more complete picture for investors. Furthermore, they can influence the risk and return profile of your bond holdings.

Credit Risk (Default Risk)

Specifically, credit risk refers to the likelihood that the bond issuer will default on its payments. Governments or companies with higher credit ratings (e.g., AAA) are considered safer. Therefore, their bonds typically offer lower yields. Conversely, issuers with lower credit ratings must offer higher yields to attract investors, compensating them for the increased risk. Consequently, if a company’s credit rating is downgraded, its existing bond prices will likely fall.

Time to Maturity

The time remaining until a bond matures significantly affects its price sensitivity to interest rate changes. Generally, longer-term bonds are more sensitive to interest rate fluctuations than shorter-term bonds. Furthermore, a small change in interest rates can have a more pronounced effect on the price of a bond maturing in 20 years versus one maturing in 2 years. This is because the fixed coupon payment represents a larger proportion of the bond’s remaining life. Reuters offers further insights into market movements.

Inflation Expectations

Inflation erodes the purchasing power of future interest payments. Therefore, if investors expect higher inflation, they demand higher yields on bonds to compensate for this loss. Consequently, existing bonds with lower fixed coupon rates become less attractive. This pressure can push their prices down. In addition, unexpected inflation can significantly impact real returns.

Supply and Demand

Like any other financial instrument, bond prices are also subject to the forces of supply and demand. If there is high demand for a particular bond, its price will rise. Conversely, if many investors are selling, prices will fall. Economic outlook, investor sentiment, and global events can all influence these dynamics. Indeed, investor behavior plays a crucial role. Bloomberg provides extensive coverage on global financial markets.

Implications for Investors

The bond prices and interest rates relationship has several practical implications for investors. Understanding these dynamics can help you make informed decisions about your fixed-income portfolio. Therefore, consider how your investment strategy aligns with current market conditions.

Long-Term vs. Short-Term Bonds

As mentioned, longer-term bonds are more sensitive to interest rate changes. If you anticipate interest rates to rise, investing in shorter-term bonds might be a safer option. Specifically, their prices will fluctuate less. Conversely, if you expect rates to fall, long-term bonds could offer greater potential for capital appreciation. Thus, matching bond duration to your interest rate outlook is wise.

Impact on Bond Funds and ETFs

Many investors hold bonds through mutual funds or exchange-traded funds (ETFs). These funds hold a diversified portfolio of bonds. Consequently, their Net Asset Value (NAV) is directly affected by changes in the underlying bond prices. Therefore, when interest rates rise, bond fund values typically decline, and vice versa. This demonstrates the broad impact of interest rate movements. The Wall Street Journal offers analysis on investment funds.

Diversification and Portfolio Strategy

Bonds often serve as a diversifier in a balanced investment portfolio. Specifically, they can provide stability during periods of stock market volatility. Understanding the bond prices and interest rates relationship allows you to adjust your bond allocation. For instance, you might reduce exposure to long-term bonds when rates are expected to climb. Indeed, thoughtful portfolio construction is key. Investopedia offers great resources for understanding investment principles. The Financial Times also provides in-depth market commentary.

Conclusion

In summary, the bond prices and interest rates relationship is fundamentally inverse. When interest rates go up, existing bond prices tend to fall, and when interest rates go down, bond prices tend to rise. This occurs because investors constantly compare the fixed coupon payments of existing bonds with the yields available on newly issued bonds. Therefore, to remain competitive, the price of older bonds must adjust. Consequently, mastering this concept is vital for navigating the fixed-income market successfully. By understanding how these forces interact, beginner investors can build more resilient portfolios and make more informed decisions about their bond investments. Indeed, knowledge is power in the world of finance.