Introduction

When you apply for a major loan, like a mortgage or a car loan, you probably know that lenders will check your credit score. However, there is another number that is just as important in their decision-making process. This number is your Debt-to-Income ratio, or DTI. Many people have never even heard of it, yet it can be the key that unlocks the door to their financial goals.

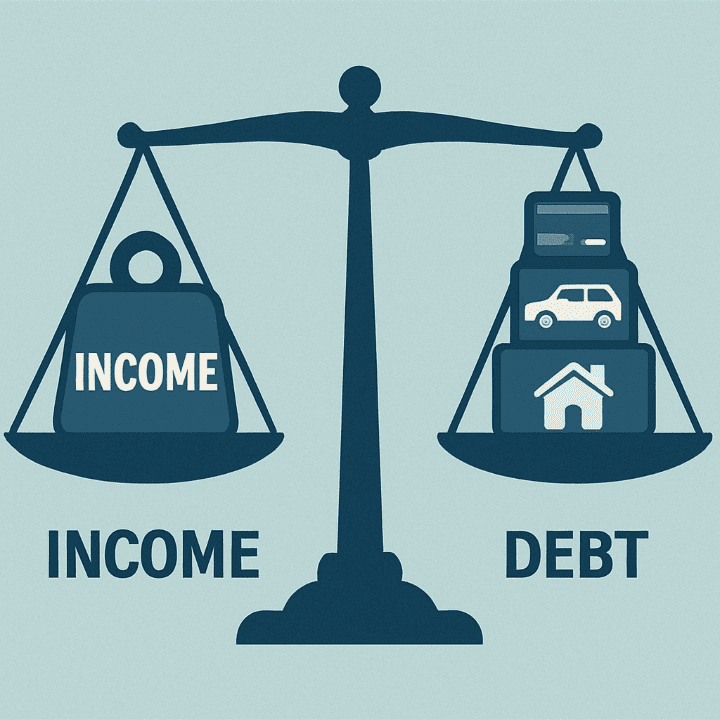

In simple terms, your DTI is a percentage. It compares the total of your monthly debt payments to your total monthly income. Lenders use it to quickly gauge your ability to comfortably afford a new loan payment. This guide will teach you everything you need to know about this crucial metric. First, we will show you how to calculate it. Then, we will explain what lenders are looking for. Finally, we will provide a clear plan to improve it.

What is Debt-to-Income (DTI) Ratio? A Simple Breakdown

Let’s define the term clearly. Your DTI ratio is a measure of your ability to manage the monthly payments you make to repay the money you have borrowed. Lenders see it as a reliable indicator of your financial health. A low DTI shows you have a good balance between your debt and your income. A high DTI, on the other hand, can suggest that you are overextended.

The formula to calculate it is very straightforward: (Total Monthly Debt Payments / Gross Monthly Income) x 100 = DTI Ratio %

What Counts as “Debt”?

For this calculation, you should add up all of your minimum required monthly debt payments. This typically includes:

- Your rent or monthly mortgage payment.

- Minimum payments on all of your credit card accounts.

- Auto loan payments.

- Student loan payments.

- Any other personal loan or alimony payments.

What Counts as “Income”?

This is a very important detail. Lenders use your gross monthly income for this calculation. This is your total income for the month before any taxes or other deductions are taken out of your paycheck.

Let’s use a quick example. Imagine your gross monthly income is $5,000. Your monthly debt payments are: $1,200 for rent, $300 for a car loan, $200 for student loans, and $100 in minimum credit card payments. Your total monthly debt is $1,800. Your DTI would be 36% ($1,800 / $5,000 = 0.36).

Why Lenders Care So Much About Your DTI

Now, why is this percentage so important to lenders? From their perspective, your DTI is a direct measure of risk. A person with a high DTI is dedicating a large portion of their monthly income just to cover their existing debts. This leaves very little room in their budget for unexpected expenses or for a new loan payment.

A low DTI, in contrast, tells the lender a different story. It shows that the borrower has a healthy amount of cash flow left over each month after paying their bills. This person is in a much stronger position to handle a new loan payment without financial strain. This is why your DTI is one of the most critical factors in getting approved for new financing. It directly answers the lender’s main question: “Does this person have the capacity to take on more debt?”

What is a “Good” DTI Ratio?

Lenders have general benchmarks that they use to evaluate your DTI. Understanding these ranges can help you see where you stand.

- 36% or less: This is generally considered the ideal range. Lenders see you as a low-risk borrower. You will likely be a strong candidate for new loans at a favorable interest rate.

- 37% to 43%: This range is considered manageable. You can still likely get approved for a loan. However, you may not be offered the best possible terms. Lenders might see you as having a slightly elevated risk.

- 44% to 50%: This is considered a high DTI. At this level, lenders become much more cautious. You will likely find it difficult to get approved for new financing.

- Over 50%: Lenders generally see this as a major red flag. It indicates a very high risk, and most lenders will not approve a new loan application.

It is also important to note that for mortgages specifically, most lenders have a strict cutoff. They typically look for a DTI ratio of 43% or less to approve a home loan.

A Step-by-Step Guide to Improving Your DTI Ratio

If your DTI is higher than you would like, do not panic. You have the power to change it. There are only two ways to improve your ratio. You must either decrease your total monthly debt payments or increase your gross monthly income. Here are some strategies.

Strategy 1: Aggressively Pay Down Your Debts

This is usually the most direct and effective approach. You should focus on reducing or eliminating your existing monthly payments. For example, paying off a credit card in full removes that minimum payment from your DTI calculation entirely. This can have a quick and positive impact. Paying extra on your car or student loans can also help you pay them off faster, eventually freeing up that cash flow.

Strategy 2: Avoid Taking on New Debt

Next, you should be very careful about adding any new monthly payments. This is especially true if you are planning to apply for a major loan, like a mortgage, in the near future. For instance, you should postpone financing a new car or making a large purchase on a credit card until after your mortgage is approved.

Strategy 3: Increase Your Income

You can also work on the other side of the equation. You can look for ways to boost your gross monthly income. This could involve asking for a raise at your current job. It could also mean taking on a side hustle or starting a small freelance business. Every extra dollar you earn helps to lower your DTI percentage.

Strategy 4: Keep Your Major Expenses Stable

Finally, a common mistake is to increase your debts as soon as your income goes up. For example, you get a raise and you immediately go out and finance a more expensive car. While you can afford the new payment, this action keeps your DTI ratio stagnant. To make real progress, you should try to keep your expenses the same while your income grows.

DTI and Your Overall Financial Health

Your DTI ratio is a vital indicator of your overall financial health. A low DTI means you have less financial stress. It also means you have more flexibility in your budget. This allows more of your money to go toward your most important goals, such as saving, investing, or travel. Your DTI and your credit score work together. Improving both is the key to mastering your financial life. Even managing smaller costs like your insurance premiums can help keep your monthly obligations low and your DTI in a healthy range.

Conclusion

In conclusion, your Debt-to-Income ratio is one of the most important numbers in your financial life. It is a powerful metric that lenders use. It is also a clear indicator of your own financial stability.

The good news is that you can calculate it easily. A lower DTI is always the goal. You can improve your ratio by consistently paying down your debts and looking for ways to increase your income.

By understanding and actively managing your DTI, you are essentially seeing your finances through the eyes of a lender. This knowledge empowers you. It helps you build a stronger financial profile. Ultimately, it is a key that helps you unlock and achieve your biggest financial goals.