Introduction

What does it truly mean to be “wealthy”? Our culture often associates wealth with a high income or lavish spending. However, these things can be misleading. True financial health is measured by a much more meaningful and accurate number: your net worth. Think of your net worth as your personal financial scorecard. It provides a clear and honest snapshot of your financial position at any given moment. It is the single most important metric for tracking your progress over time.

This guide is designed to demystify this powerful concept. Many people think tracking net worth is only for the rich, but that is simply not true. It is a vital tool for everyone. First, we will show you exactly how to calculate it. Then, we will explore practical, actionable strategies you can use to make that number grow consistently.

What is Net Worth and Why Does It Matter?

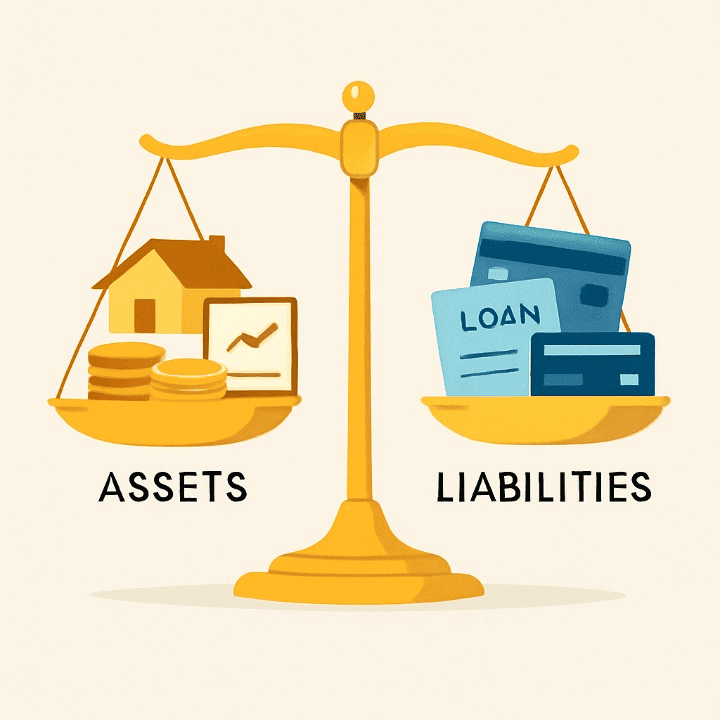

The definition of net worth is surprisingly simple. It is the value of everything you own minus the value of everything you owe. The formula looks like this:

Assets (what you own) – Liabilities (what you owe) = Net Worth

Let’s break down those two components. Assets are resources with economic value. This includes cash in your bank accounts, investments, real estate, and valuable personal property. Liabilities, on the other hand, are your financial obligations or debts. This includes your mortgage, car loan, student loans, and any outstanding credit card balances.

So, why does this number matter more than your income? A person can earn a very high salary but also have massive debts. As a result, they could have a low or even a negative net worth. Conversely, someone with a modest income who saves and invests diligently can build a very high net worth over time. This makes it the truest measure of your financial progress. Furthermore, a strong and growing net worth is a key factor that lenders consider when you apply for major financing.

How to Calculate Your Net Worth: A Step-by-Step Guide

This exercise is practical and empowering. You should plan to do it at least once a year to track your progress. Here’s how to do it step-by-step.

Step 1: List All Your Assets

First, you need to add up the value of everything you own. It helps to break this down into categories for clarity.

- Cash and Equivalents: This is your most liquid money. Include balances from your checking accounts, savings accounts, and any money market funds.

- Investments: List the current market value of all your investment accounts. This includes retirement accounts like a 401(k) or an IRA, as well as any taxable brokerage accounts with stocks, bonds, or mutual funds.

- Real Estate: If you own a home, find its current estimated market value. You can use online real estate tools for a reasonable estimate.

- Personal Property: Include the resale value (not the price you paid) of your most valuable possessions. This typically includes your car. Other items like jewelry or collectibles can also be included if they have significant value.

- Other Assets: Some forms of permanent life insurance build up a “cash value” over time. If your policy has this feature, you can include that cash value as an asset.

Step 2: List All Your Liabilities

Next, you need to create a complete list of all your debts.

- Secured Debt: This debt is tied to a specific asset. The most common examples are your mortgage balance and any outstanding auto loans.

- Unsecured Debt: This debt is not backed by an asset. This category includes all of your credit card balances, student loans, personal loans, and any medical debt.

Step 3: Do the Simple Math

Finally, add up your total assets. Then, add up your total liabilities. Subtract your total liabilities from your total assets. The result is your current net worth. Don’t be discouraged if the number is low or even negative, especially if you are young or have student loans. The important thing is not where you start. The important thing is to know your number and have a plan to improve it.

Strategies to Grow Your Net Worth

There are only two fundamental ways to increase your net worth. You can either increase your assets or decrease your liabilities. The most effective financial management strategies do both at the same time.

Strategy 1: Aggressively Reduce Liabilities

First, focus on paying down your debts, especially high-interest debt. Every dollar you use to pay off a credit card with a high interest rate provides a guaranteed return on your money equal to that rate. For example, paying off a card with a 20% interest rate is like earning a 20% return on your money. This has an immediate and powerful impact on your net worth.

Strategy 2: Consistently Increase Assets

Second, you need to build the habit of saving and investing. The most effective way to do this is through automation. You should set up automatic transfers from your checking account to your savings and investment accounts every payday. This “pay yourself first” approach ensures that you are consistently building your assets over time. Your investments then grow not just from your contributions, but also from compound growth, where your earnings start generating their own earnings.

Strategy 3: Boost Your Income

Finally, you can accelerate your net worth growth by increasing your income. You could pursue a raise at your current job, develop new skills, or start a side hustle. Every extra dollar you earn provides more capital. You can then use this capital to either pay down liabilities faster or purchase more assets.

Your Net Worth and Your Financial Future

Tracking and growing your net worth has profound long-term benefits. A consistently growing net worth demonstrates financial responsibility. This, in turn, improves your overall credit profile and makes you appear less risky to lenders. As a result, it becomes much easier to get approved for financing for a future home or business. You will also likely be offered a more favorable interest rate.

Ultimately, focusing on this single metric is the most effective way to manage your overall financial health. It keeps you focused on the big picture. It helps ensure that your daily financial decisions are leading you toward a future of security, freedom, and true wealth.

Conclusion

In conclusion, your net worth is your ultimate financial scorecard. It provides a clear, honest picture of your progress. Calculating it is a simple exercise. You just need to list what you own and what you owe. From there, growing it involves a dedicated, two-pronged attack. You must work to reduce your debts while also consistently increasing your assets.

Do not be discouraged by your starting number. Many financially successful people began with a negative net worth. The most important thing is to know your score and to have a clear plan. By tracking this metric year after year, you can ensure that you are always moving in the right direction. You will be on the path to building true, lasting wealth and achieving financial peace of mind.