Understanding the effect of inflation on real interest rates is paramount for any diligent saver or investor. Inflation, often dubbed the “silent thief,” constantly works to diminish the purchasing power of your money over time. Consequently, this economic phenomenon directly impacts the true return you earn on your savings, making it crucial to grasp its intricate relationship with interest rates. Effectively managing your finances necessitates a clear comprehension of how inflation erodes your wealth and what steps you can take to mitigate its effects.

Unpacking the Basics: What Are Inflation and Interest Rates?

Defining Inflation

Inflation signifies the rate at which the general level of prices for goods and services is rising, and subsequently, the purchasing power of currency is falling. Imagine a loaf of bread costing $2 today. If inflation is 5%, that same loaf might cost $2.10 next year. This erosion of purchasing power affects everything from daily necessities to long-term investments.

Economists typically measure inflation using various indices, with the Consumer Price Index (CPI) being one of the most common. The CPI tracks changes in the prices of a basket of consumer goods and services purchased by urban consumers. Therefore, a rising CPI indicates increasing inflation. High inflation can severely impact household budgets and financial planning, demanding careful consideration from policymakers and individuals alike.

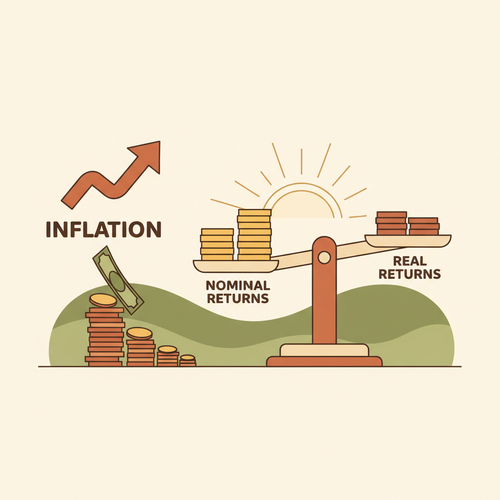

Nominal vs. Real Interest Rates

Interest rates represent the cost of borrowing money or the return for lending it. However, not all interest rates are created equal when viewed through the lens of inflation. We must differentiate between nominal and real interest rates.

The nominal interest rate is the stated rate on a loan or investment. It is the percentage return you see advertised on a savings account or bond. For instance, if your savings account offers a 2% annual interest rate, 2% is the nominal rate. This figure does not account for any changes in purchasing power due to inflation.

Conversely, the real interest rate reflects the true return on your investment after accounting for inflation. It provides a more accurate picture of how your purchasing power is actually growing or shrinking. It is the nominal rate adjusted for the rate of inflation. Understanding this distinction is fundamental for making informed financial decisions, as it reveals the genuine economic benefit of your returns.

The Direct Link: How Inflation Shapes Real Interest Rates

The relationship between inflation and real interest rates is often best explained by the Fisher Equation, a fundamental concept in economics. This equation states that the real interest rate is approximately equal to the nominal interest rate minus the inflation rate. In simple terms: Real Interest Rate = Nominal Interest Rate – Inflation Rate. This formula highlights how inflation directly subtracts from the apparent gains of your investments.

Consider a scenario where your savings account offers a 3% nominal interest rate. If inflation is also 3%, your real interest rate is 0%. Consequently, while your money balance increases, its ability to buy goods and services remains unchanged. Your purchasing power has not grown at all. This situation means your money is merely treading water, failing to generate any real wealth.

Furthermore, if inflation rises above your nominal interest rate, your real interest rate becomes negative. For example, a 2% nominal interest rate combined with 4% inflation results in a -2% real interest rate. In this alarming scenario, your savings are losing purchasing power over time, even as your account balance numerically increases. Therefore, investors must always seek a positive real return to genuinely grow their wealth. Investopedia provides an excellent deep dive into the Fisher Effect.

The Impact on Your Savings Returns

Erosion of Purchasing Power

The most immediate and concerning impact of inflation on your savings returns is the erosion of purchasing power. Many traditional savings vehicles, such as basic savings accounts or money market accounts, often offer nominal interest rates that are relatively low. During periods of high or even moderate inflation, these rates frequently fall below the inflation rate.

Consequently, your money, though earning some interest, buys less and less each year. Over the long term, this phenomenon can significantly diminish the value of your accumulated wealth. A sum of money that could afford a comfortable retirement today might be insufficient in 20 or 30 years if inflation continues to outpace your returns. This makes the quest for returns that beat inflation absolutely essential for preserving and growing your financial future.

Think about a fixed-income investment, like a Certificate of Deposit (CD), offering a guaranteed 1.5% nominal return for five years. If average inflation over that period is 2.5%, your real return is -1%. This means that after five years, the purchasing power of your money has actually decreased, despite earning interest. This silent decline can catch many savers by surprise, highlighting the need for a deeper understanding of real returns.

The Quest for Positive Real Returns

Given the constant threat of inflation, investors are perpetually on a quest for positive real returns. This involves identifying and allocating capital to assets that historically have demonstrated the ability to outpace inflation. Simply put, you want your investments to grow at a rate higher than the rate at which prices are increasing.

Various asset classes offer different potentials for achieving this goal. Equities (stocks), for instance, often provide a hedge against inflation because companies can potentially increase their prices and revenues in an inflationary environment. Real estate can also serve as an inflation hedge, with property values and rental income tending to rise with general price levels. Reuters often reports on market trends affecting inflation-protected securities.

However, no single investment guarantees positive real returns. Each asset class carries its own risks and rewards. Therefore, a diversified approach is usually recommended, ensuring your portfolio is robust enough to withstand various economic conditions, including inflationary pressures. The goal remains to ensure your money works harder than inflation itself.

Strategies to Safeguard Your Wealth Against Inflation

Diversification is Key

One of the most effective strategies to protect your wealth from the adverse effects of inflation is diversification. Spreading your investments across various asset classes helps to mitigate risk and potentially capture returns from different sectors of the economy. A well-diversified portfolio might include a mix of stocks, bonds, real estate, and commodities.

Certain asset classes historically perform better during inflationary periods. For example, commodities like gold, oil, and other raw materials often see their prices rise as inflation accelerates. Therefore, including a small allocation to such assets can act as a natural hedge. Furthermore, diversifying across different industries and geographies can further shield your portfolio from localized economic shocks.

Consider Inflation-Protected Securities

For investors seeking a direct hedge against inflation, Treasury Inflation-Protected Securities (TIPS) are a highly effective option. These government-issued bonds are designed to protect investors from the erosion of purchasing power. The principal value of a TIPS bond adjusts with inflation, as measured by the Consumer Price Index (CPI).

When inflation rises, the principal value of your TIPS increases, and consequently, the interest payments you receive also increase (since they are a fixed percentage of the adjusted principal). If deflation occurs, the principal value can decrease, but it is guaranteed not to fall below its original face value at maturity. This feature makes TIPS a powerful tool for preserving real capital, particularly for those with a lower risk tolerance. The U.S. Department of the Treasury provides comprehensive information on TIPS.

Invest in Productive Assets

Investing in productive assets can be a robust long-term strategy against inflation. Productive assets are those that generate income or grow in value over time. Stocks of companies that possess strong pricing power, meaning they can pass increased costs to consumers without significant loss of sales, tend to perform well during inflationary times.

Real estate, particularly income-producing properties, also falls into this category. Rental income can typically be adjusted upwards with inflation, and property values often appreciate, providing a dual benefit. Businesses and real estate are tangible assets that can adapt to changing economic conditions, unlike cash, which simply loses value. Therefore, allocating capital to these assets can help your wealth grow in real terms.

Re-evaluate Your Savings Vehicles

Regularly re-evaluating where you keep your emergency funds and short-term savings is a critical step in combating inflation. While traditional savings accounts offer liquidity, their low-interest rates often lead to negative real returns during inflationary periods. Consider exploring higher-yield savings accounts or short-term Certificates of Deposit (CDs) with competitive rates.

Although these options might not always beat inflation, they can minimize the loss of purchasing power compared to standard accounts. For longer-term savings, consider moving beyond cash and into diversified investment portfolios designed to generate higher real returns. Ultimately, being proactive about where your money resides can significantly impact its future value.

Conclusion

The intricate relationship between inflation and real interest rates is a cornerstone of personal finance. Understanding the effect of inflation on real interest rates is not merely an academic exercise; it is an essential skill for protecting and growing your financial future. Inflation relentlessly erodes the purchasing power of your savings, often turning seemingly positive nominal returns into real losses. By grasping the difference between nominal and real interest rates, you gain a powerful lens through which to view your investments.

Consequently, a proactive approach to financial planning becomes imperative. Diversifying your portfolio, exploring inflation-protected securities like TIPS, and investing in productive assets are all viable strategies to combat the silent erosion of wealth. Ultimately, staying informed and adapting your financial strategy to the prevailing economic climate will empower you to safeguard your savings and ensure your money maintains its value over time.