A CD laddering strategy represents a powerful and often underestimated approach for investors seeking to maximize returns and manage risk in dynamic interest rate environments. This intelligent technique allows individuals to harness the stability of Certificates of Deposit (CDs) while maintaining a degree of liquidity and adapting to market shifts. Consequently, understanding how to effectively implement a CD ladder can significantly enhance your fixed-income portfolio, offering both predictable income and growth potential. This article will delve into the mechanics, benefits, and practical steps of building a successful CD ladder, ensuring you are well-equipped to navigate today’s financial landscape.

Understanding Certificates of Deposit (CDs)

What is a CD?

A Certificate of Deposit, commonly known as a CD, is a type of savings account that holds a fixed amount of money for a fixed period of time, such as six months, one year, or five years. Financial institutions issue these products, offering a fixed interest rate in return for your commitment not to withdraw the funds before the maturity date. Generally, higher interest rates accompany longer terms, compensating you for the extended lock-up period. Moreover, the Federal Deposit Insurance Corporation (FDIC) or the National Credit Union Administration (NCUA) insures CDs, making them an extremely low-risk investment option. This insurance protects your principal up to specified limits, typically $250,000 per depositor, per insured bank, per ownership category. Therefore, CDs provide a secure avenue for capital preservation.

Benefits and Drawbacks of Traditional CDs

Traditional CDs offer several compelling benefits for investors. Firstly, their fixed interest rates provide predictable income streams, simplifying financial planning. Secondly, the FDIC insurance guarantees the safety of your principal, offering peace of mind. Thirdly, CDs are straightforward investment vehicles, making them accessible even for novice investors. They require minimal management once established.

However, traditional CDs also come with certain drawbacks. Primarily, their fixed nature means you sacrifice liquidity; withdrawing funds before maturity often incurs significant penalties. This can be problematic if you need access to your capital unexpectedly. Additionally, in an environment of rising interest rates, money locked into a low-yielding CD will miss out on potentially higher returns elsewhere. Conversely, if rates fall, locking in a high rate can be advantageous. Consequently, investors must carefully consider their financial needs and market outlook before committing to a traditional CD.

Why CDs Matter in Today’s Market

In today’s often volatile financial markets, CDs offer a sanctuary of stability. Investors frequently seek safe havens amidst stock market fluctuations or economic uncertainty. CDs fulfill this role admirably, providing guaranteed returns without the inherent risks of equities. Furthermore, as central banks adjust monetary policy, interest rates can become a significant factor in investment decisions. During periods of rising rates, CDs become increasingly attractive, offering more competitive yields compared to traditional savings accounts. Thus, incorporating CDs into a diversified portfolio can act as a crucial stabilizing element, preserving capital while generating steady income.

The CD Laddering Strategy Explained

What is CD Laddering?

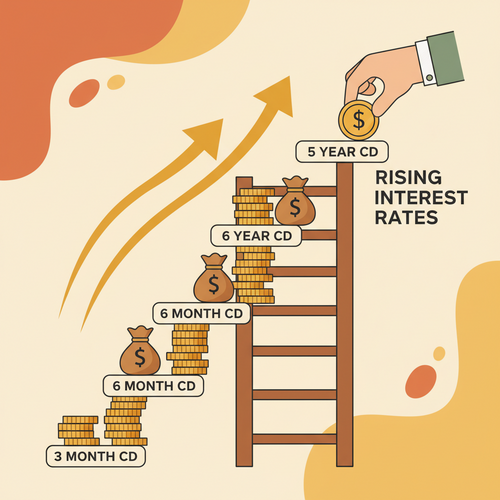

The CD laddering strategy involves dividing a lump sum of money into several smaller portions and investing each portion in CDs with different maturity dates. Instead of placing all your funds into a single CD with one maturity term, you spread your investment across a range of terms. For example, you might invest in CDs maturing in one, two, three, four, and five years. As a result, this creates a “ladder” of maturities, where one CD matures at regular intervals.

How Does a CD Ladder Work?

Let’s illustrate how a CD ladder operates in practice. Imagine you have $25,000 to invest. With a five-year CD ladder, you might allocate $5,000 to a 1-year CD, $5,000 to a 2-year CD, $5,000 to a 3-year CD, $5,000 to a 4-year CD, and the remaining $5,000 to a 5-year CD. Each year, one of your CDs matures. When the 1-year CD matures, you then have a choice: you can either withdraw the money if needed or, more commonly, reinvest it into a new 5-year CD.

By consistently reinvesting the maturing CD into the longest term available in your ladder, you maintain a continuous stream of maturing funds. This ensures that you always have a portion of your money becoming accessible, typically once a year. Consequently, you are continually rolling over funds into potentially higher-yielding, longer-term CDs. This systematic reinvestment process is the core mechanism of the CD ladder.

Key Advantages of CD Laddering

Implementing a CD ladder offers a multi-faceted approach to optimizing your CD investments. Firstly, it significantly enhances liquidity. While individual CDs lock up funds, the ladder structure ensures that a portion of your money becomes available periodically. This eliminates the “all or nothing” dilemma of a single, long-term CD. Secondly, it allows you to capture higher interest rates. Longer-term CDs typically offer better yields, and by continually reinvesting into the longest rung of your ladder, you consistently benefit from these elevated rates over time.

Furthermore, a CD ladder provides crucial protection against interest rate fluctuations. If rates rise, you can reinvest your maturing CD at the new, higher rate. Conversely, if rates fall, you still have some funds locked into older, higher-yielding CDs, cushioning the impact. This diversification across maturities smooths out the effects of changing rates. Therefore, a CD ladder blends the best aspects of short-term liquidity with long-term earning potential, making it an incredibly versatile strategy for fixed-income investors.

Building Your CD Ladder: A Step-by-Step Guide

Constructing a CD ladder is a relatively straightforward process, yet it requires careful planning to align with your financial goals. Following these steps will help you establish an effective and resilient ladder.

Step 1: Determine Your Investment Amount and Time Horizon

Before initiating your CD ladder, assess the total amount of money you wish to allocate to this strategy. This initial capital should be funds you don’t anticipate needing immediately, although the ladder provides periodic liquidity. Additionally, define your investment time horizon. Do you envision a 3-year, 5-year, or even a 10-year ladder? Your time horizon will influence the range of CD terms you select for your ladder. For instance, a longer time horizon might incorporate CDs with terms up to 7 or 10 years, potentially offering higher yields. This crucial first step lays the foundation for your entire ladder structure.

Step 2: Choose Your CD Terms

Once you have your total investment amount, decide on the specific CD terms you will use. A common approach for a beginner is to use equally spaced maturities, such as 1-year, 2-year, 3-year, 4-year, and 5-year CDs. This creates a balanced ladder, ensuring annual access to funds. However, you can customize this based on market conditions or your liquidity needs. Perhaps you need more frequent access; therefore, you could use 3-month, 6-month, 9-month, and 12-month CDs. Conversely, if you prioritize higher rates and have less immediate liquidity concern, you might opt for a ladder with longer increments, like 2-year, 4-year, 6-year, 8-year, and 10-year CDs. Flexibility is a key feature of this strategy.

Step 3: Stagger Your Maturities

With your investment amount and chosen terms, divide your total capital into equal segments, each corresponding to a different maturity term. For a $25,000 investment with a 5-year ladder (1-5 years), you would invest $5,000 in each term. Secure these CDs from a reputable financial institution, preferably one offering competitive rates and FDIC insurance. It is often beneficial to compare rates across multiple banks or credit unions to ensure you are getting the best possible return. Many online banks frequently offer superior CD rates compared to traditional brick-and-mortar institutions. Therefore, research is paramount in this phase.

Step 4: Reinvest and Adapt

The true power of the CD ladder manifests in its ongoing management. As each CD matures, you have a critical decision point. If you require the funds, you can withdraw them without penalty. However, to maintain the ladder, you should reinvest the maturing principal into a new CD with the longest available term in your ladder. For example, when your 1-year CD matures, you reinvest it into a new 5-year CD. This action effectively “rolls” your ladder forward, ensuring that you always have a CD maturing each year while consistently chasing the highest long-term rates. Regularly review your ladder and adjust it as your financial situation or market conditions change.

Navigating Fluctuating Interest Rates with a CD Ladder

The primary allure of the CD laddering strategy lies in its inherent ability to mitigate the risks associated with unpredictable interest rate movements. This dynamic adaptability makes it an invaluable tool for fixed-income investors.

Protecting Against Rate Declines

Imagine a scenario where interest rates are steadily falling. If you had invested all your capital in a single, short-term CD, you would be forced to reinvest at progressively lower rates upon maturity, severely impacting your overall returns. However, with a CD ladder, a significant portion of your funds is locked into longer-term CDs. These longer-term CDs typically offer higher rates that are fixed for several years. Consequently, even as new rates decline, your ladder provides a protective shield, as only a fraction of your portfolio matures at any given time, allowing you to retain some of those advantageous older rates. This staggered approach safeguards your income stream.

Benefiting from Rate Increases

Conversely, consider an environment of rising interest rates. If you had committed all your funds to a single, long-term CD at a low rate, you would be stuck, missing out on the opportunity to earn more. A CD ladder, however, allows you to capitalize on these upward movements. As your shorter-term CDs mature, you can reinvest that principal into new, longer-term CDs at the now higher prevailing rates. This continuous reinvestment at favorable rates allows your overall portfolio yield to gradually increase over time. Thus, the ladder ensures you are never entirely locked into low rates during a rising rate cycle, providing constant opportunities for yield improvement.

Liquidity and Flexibility

Beyond interest rate management, a CD ladder inherently offers enhanced liquidity compared to holding a single, long-term CD. Since a portion of your investment matures at regular intervals, you gain predictable access to funds. This periodic liquidity is particularly beneficial for investors who might need a portion of their capital for specific expenses or opportunities but still wish to benefit from the higher rates of longer-term deposits. Furthermore, this strategy provides remarkable flexibility. If your financial needs change, you can choose not to reinvest a maturing CD and instead use the funds. This adaptability makes the CD ladder a prudent choice for those who value both stability and access to their money.

Advanced Considerations and Best Practices

To maximize the effectiveness of your CD laddering strategy, it’s important to delve into some advanced considerations and employ best practices. These insights can further refine your approach and optimize your returns.

CD Types and Their Role in Laddering

While traditional fixed-rate CDs form the backbone of most ladders, other CD types can also play a role. Callable CDs, for instance, allow the issuing bank to redeem the CD before its maturity date, usually if interest rates fall significantly. These often offer higher rates as compensation for the call risk. Brokered CDs are purchased through a brokerage firm and can sometimes offer better rates or a wider range of maturities. However, they may carry different liquidity characteristics. Additionally, “No-Penalty” or “Liquid” CDs allow withdrawals without penalty after a certain initial period, offering maximum flexibility at the cost of slightly lower rates. Consider how these specialized CDs might fit into your overall ladder structure based on your risk tolerance and liquidity needs. Carefully research any non-traditional CD types before incorporating them into your strategy. More information on different CD types can be found on reputable financial education sites like Investopedia.

Tax Implications of CD Investments

Understanding the tax implications of your CD ladder is crucial for accurate financial planning. The interest earned on CDs is generally taxable at the federal, state, and local levels. For most individual investors, this interest income is taxed as ordinary income in the year it is credited or made available to you, even if you reinvest it. Therefore, if you have a significant CD ladder, the accumulated interest can increase your taxable income. Consider holding CDs in tax-advantaged accounts like an Individual Retirement Account (IRA) if eligible. This allows your interest to grow tax-deferred or, in the case of a Roth IRA, potentially tax-free. Always consult a qualified tax professional to understand your specific tax situation and optimize your CD investments. The Internal Revenue Service (IRS) website provides extensive resources on investment income taxation.

Comparing CD Ladders to Other Fixed-Income Options

A CD ladder is an excellent tool, but it’s essential to view it within the broader context of other fixed-income investment options. For example, short-term Treasury bills offer exceptional safety backed by the U.S. government, often at competitive rates, and are exempt from state and local taxes. Money market accounts provide high liquidity but typically offer lower yields. Bond funds or individual bonds can offer potentially higher returns, but they also carry interest rate risk and credit risk, especially corporate bonds.

When evaluating a CD ladder against these alternatives, consider your specific risk tolerance, liquidity requirements, and return expectations. The CD ladder excels in offering a balanced approach: enhanced liquidity compared to a single long-term CD, superior rates compared to standard savings accounts, and lower risk than most bond investments. It serves as a middle-ground solution, providing a compelling blend of safety, income, and adaptability. Resources from the Federal Reserve can offer insights into broader economic and interest rate trends affecting all fixed-income investments.

Conclusion

The CD laddering strategy stands out as a sophisticated yet accessible method for investors to optimize their returns from Certificates of Deposit. By systematically staggering maturity dates, individuals can effectively navigate fluctuating interest rate environments, ensuring both consistent liquidity and the ability to capture higher yields. This strategic approach mitigates the common drawbacks of traditional CDs, transforming them into a more dynamic and responsive investment vehicle. Whether rates are rising or falling, a well-constructed CD ladder provides a robust defense and opportunistic advantage. Therefore, for those seeking to maximize capital preservation and generate reliable income within their fixed-income portfolio, understanding and implementing a CD ladder is an undeniably smart financial move. It truly offers a blend of safety, accessibility, and growth potential that few other low-risk options can match.