Introduction

When you navigate the world of personal finance, it can feel like you’re drowning in an alphabet soup of acronyms: IRA, ETF, FICO, and two of the most common yet confusing terms—APR and APY. You see them advertised for credit cards, auto loans, and high-yield savings accounts. They both relate to interest rates, but they tell very different stories about your money. Is a 5% APR the same as a 5% APY? The short answer is no, and not understanding the difference can cost you hundreds or even thousands of dollars over time.

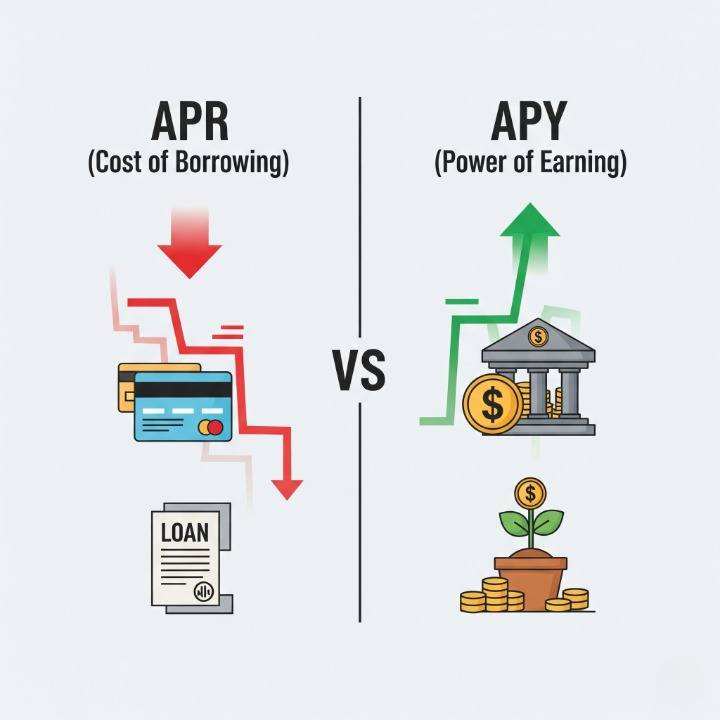

Think of APR and APY as two sides of the same coin: one measures the cost of borrowing money, while the other measures the power of earning it. Mistaking one for the other is a common pitfall that can lead to paying more on loans or earning less on your savings. This guide will demystify the APR vs. APY debate once and for all. We’ll break down what each term means in simple language, explain the critical difference between them, and show you how to use this knowledge to make smarter financial decisions, whether you’re taking out a loan or growing your savings from your online business.

What is APR (Annual Percentage Rate)? The True Cost of Borrowing

The Annual Percentage Rate (APR) represents the total yearly cost you pay to borrow money. It’s the most important number to look at when you’re considering a loan or a credit card.

Think of it as the “full price tag” for borrowing. It doesn’t just include the interest rate; it also bundles in most of the fees associated with the loan, such as origination fees, closing costs, or administrative charges. This is why the APR is often slightly higher than the advertised “headline” interest rate. The law requires lenders to disclose the APR so that consumers can make fair, apples-to-apples comparisons between different loan offers.

You will find APR on products where you owe money, such as:

- Credit Cards

- Mortgages

- Auto Loans

- Personal Loans

- Student Loans

When you see a low APR, it means the cost of borrowing is lower. A 3% APR on a car loan is significantly better than a 7% APR. For credit cards, the APR is the rate charged on any balance you don’t pay off by the due date.

What is APY (Annual Percentage Yield)? The Real Power of Earning

The Annual Percentage Yield (APY), on the other hand, represents the total amount of interest you earn on a deposit account over a year. It’s the number you want to focus on when you’re saving or investing your money.

Think of APY as your “total take-home profit” from a savings product. The magic ingredient that makes APY so powerful—and different from APR—is compounding. Compounding is the process of earning interest not only on your initial deposit but also on the accumulated interest from previous periods. It’s essentially “interest on your interest,” and it’s what makes your money grow faster over time.

You will find APY on products where your money works for you, such as:

- High-Yield Savings Accounts

- Certificates of Deposit (CDs)

- Money Market Accounts

When you’re saving, you want the highest APY possible. A savings account with a 4.5% APY will grow your money faster than one with a 3.5% APY.

The Key Difference: Simple vs. Compound Interest

The core of the APR vs. APY distinction boils down to one thing: compounding.

- APR generally reflects simple interest plus fees. It tells you the straightforward rate you’ll pay over a year.

- APY always accounts for compound interest. It shows you what your effective rate of return will be once the effect of compounding is included.

Let’s use a simple scenario. Meet Leo, a freelancer who just made $10,000 from a big project. He wants to save it for a year. He has two options:

- Bank A offers a “5% simple interest rate” (like an APR without fees).

- Bank B offers a “5% APY” with interest that compounds monthly.

- With Bank A: At the end of the year, Leo earns 5% of $10,000, which is $500. His total is $10,500.

- With Bank B: The bank calculates and adds interest to his balance every month. In the first month, he earns a little interest. The next month, he earns interest on his original $10,000 plus the interest from the first month. By the end of the year, this compounding effect means his total earnings will be approximately $511.62. His total is $10,511.62.

It may not seem like a huge difference, but over time and with larger amounts, compounding makes a massive impact. This is why APY is the true measure of your earning potential.

APR vs. APY in the Real World

Understanding when to look for APR and when to look for APY is key to sound personal finance.

Scenario 1: Taking Out a Personal Loan for Your Business

You’re expanding your online store and need a $5,000 loan.

- Lender X offers a 7% interest rate with a $100 origination fee.

- Lender Y offers a 7.2% interest rate with no fees.

At first glance, Lender X looks cheaper. But when you compare the APR, which includes the fee, Lender X might have an APR of 7.45%, while Lender Y’s APR is 7.2%. In this case, Lender Y is the more affordable choice. When borrowing, the lower APR wins. For more on this, the Consumer Financial Protection Bureau (CFPB) offers excellent resources.

Scenario 2: Opening a High-Yield Savings Account

- Online Bank C offers a 4.65% APY.

- Credit Union D offers a 4.75% APY.

This is a straightforward comparison. Since APY already accounts for compounding, you know that your money will grow faster at Credit Union D. When saving, the higher APY wins.

Conclusion

While APR and APY might seem like technical jargon, they are fundamental concepts that empower you to take control of your financial life. The distinction is simple when you remember their purpose:

- APR (Annual Percentage Rate) is for borrowing. It represents the total cost, and your goal is to find the lowest APR possible.

- APY (Annual Percentage Yield) is for earning. It reflects your total return with compounding, and your goal is to find the highest APY possible.

By mastering the difference between APR vs. APY, you move from being a passive consumer to an informed decision-maker. You can now confidently compare credit card offers, evaluate loan terms, and choose savings accounts that will truly maximize the growth of your hard-earned money. The next time you see these three letters, you won’t feel confused; you’ll feel confident.

Did this explanation help clear things up? Share your thoughts or questions in the comments below! And if you want to learn more about our mission to demystify finance, check out our About Us page.