Introduction

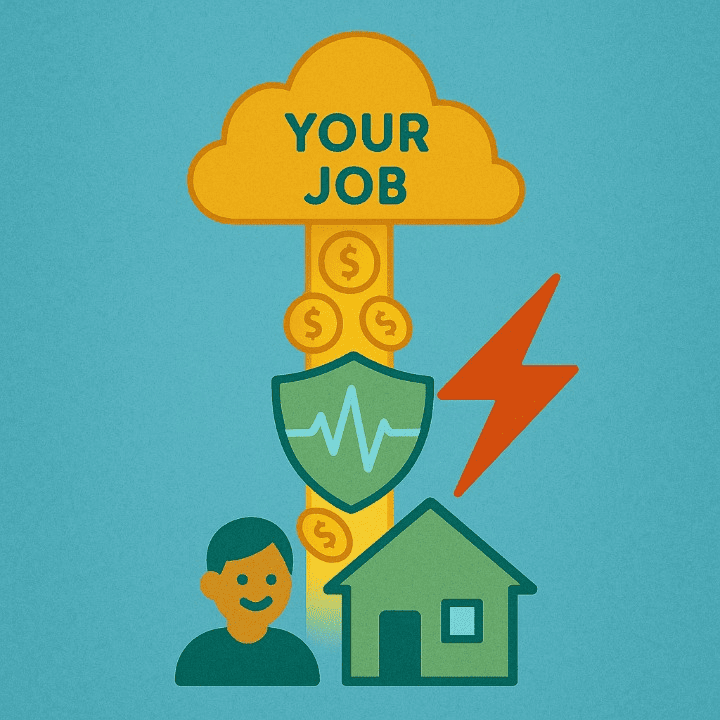

What is your single most valuable financial asset? Many people might think of their home, their car, or their investment accounts. However, for most working adults, the correct answer is much simpler. Your most valuable asset is your ability to earn an income. Your paycheck is the engine that powers your entire financial life. It pays for your housing, your food, and your future goals.

Now, ask yourself another important question. What would happen if a sudden illness or injury prevented you from working for months, or even years? This is where disability insurance comes in. It is a crucial, yet often overlooked, type of insurance. In short, it provides you with a replacement for your income when an unexpected disability stops you from being able to work. This guide will explain what it is, how it works, and why it is so essential.

The Foundation: What is Disability Insurance?

First, let’s define the term clearly. Disability insurance is a type of policy that pays you a percentage of your regular income if you are unable to work. This inability must be due to a covered illness or injury. You can think of it as “paycheck protection” or “income insurance.” Its sole purpose is to provide you with a steady stream of cash flow so you can continue to pay your bills while you recover.

Many people associate the word “disability” with catastrophic, work-related accidents. However, the reality is that most long-term disabilities are caused by common illnesses. These can include things like cancer, heart disease, or severe arthritis. Statistics show that a significant percentage of people will experience a disability that keeps them out of work for an extended period at some point during their career. This makes the risk very real and relatable for everyone.

The Two Main Types: Short-Term and Long-Term Disability

Disability insurance is generally broken down into two main categories. These categories are based on how long the policy will provide benefits.

Short-Term Disability (STD) Insurance

As its name implies, short-term disability insurance is designed to cover you for a temporary period. It is meant for disabilities that you are expected to recover from in a matter of months.

- Benefit Period: The length of time you receive payments is typically short. For example, it might last for three to six months, and rarely more than a year.

- Elimination Period: This is the waiting period before your benefits begin. For STD, this period is usually very short, often between one and two weeks after you become disabled.

- Coverage: This type of policy usually replaces a higher percentage of your income. For instance, it might cover 60% to 80% of your gross pay.

Long-Term Disability (LTD) Insurance

Long-term disability insurance, on the other hand, is designed to protect you from more serious, career-altering conditions. It provides a safety net for illnesses or injuries that could last for many years.

- Benefit Period: The benefit period for LTD is much longer. It can last for several years, such as five or ten years. Some policies will even provide benefits until you reach retirement age.

- Elimination Period: The waiting period for LTD is also much longer. It is typically 90 days or more. In fact, it is designed to begin after your short-term disability benefits have run out.

- Coverage: LTD usually replaces a smaller percentage of your income. For example, a typical policy might cover 50% to 60%. While this is a smaller percentage, it provides a stable income for a much longer and more critical period.

Decoding Your Policy: Key Terms to Understand

When you look at a disability insurance policy, you will encounter some specific terminology. It is important to understand these key terms.

Definition of Disability: First, this is the most important clause in the entire policy. It defines what it means to be “disabled.” An “own-occupation” policy is generally considered the best. It means you are eligible for benefits if you are unable to perform the duties of your specific job. In contrast, an “any-occupation” policy only pays benefits if you are unable to perform any job for which you are reasonably qualified.

Benefit Amount: This is the specific amount of money you will receive each month. This benefit is usually paid out tax-free, but you should always confirm this detail.

Elimination Period (or Waiting Period): As mentioned, this is the amount of time you must be disabled before you can receive your first payment. You can often choose your elimination period. Selecting a longer period will typically result in a lower monthly premium.

Benefit Period: Finally, this is the maximum length of time that you can receive payments from the policy for a single disability.

The Financial Consequences of Being Uninsured

Now, let’s consider the stark reality of what happens without this protection. If a disability prevents you from working, your income stops immediately. However, your expenses do not. Your mortgage or rent is still due. Your utility bills will continue to arrive. You still need to buy food for your family.

First, people are forced to drain their emergency funds. Once that money is gone, they often have to cash out their retirement savings, which can come with heavy taxes and penalties. After those funds are depleted, many people turn to high interest rate credit card debt just to cover basic living expenses.

This sequence of events can completely destroy a person’s financial life. It can ruin a good credit score. This, in turn, makes it nearly impossible to get new financing for years to come. In short, disability insurance does not just protect your paycheck. It protects your savings, your retirement, and your entire financial future.

Conclusion

In conclusion, your ability to earn an income is the engine that powers your financial life. Therefore, disability insurance is the essential tool you use to protect that engine. It provides a crucial safety net that ensures an unexpected illness or injury does not have to become a devastating financial crisis.

We have seen that there are two main types of this insurance. Short-term disability helps you navigate temporary issues. Long-term disability, on the other hand, protects you from more catastrophic events. While we can never predict what our future health holds, we can certainly prepare for it. Securing adequate disability insurance is one of the most important financial decisions you can make. It provides peace of mind and allows you to build your future with confidence.