Introduction

Navigating the world of permanent life insurance can feel like deciphering a complex financial puzzle. Among the many options, two types often stand out and spark significant discussion: Whole Life insurance and Indexed Universal Life (IUL) insurance. Both offer lifelong coverage and a cash value component, making them appealing as both protection and potential wealth-building tools. However, their mechanics, guarantees, and growth potential differ significantly.

Many investors, from beginners to those with intermediate experience, seek to understand which policy aligns best with their financial goals and risk tolerance. This article aims to demystify these two powerful financial instruments, providing a clear and comprehensive comparison. We will explore their core features, benefits, and drawbacks to help you make an informed decision for your financial future and long-term planning.

Understanding Permanent Life Insurance

What is Permanent Life Insurance?

Unlike term life insurance, which provides coverage for a specific period, permanent life insurance offers coverage for your entire life, as long as premiums are paid. It’s a dual-purpose financial product designed to provide a death benefit to your beneficiaries and accumulate cash value over time. This cash value grows on a tax-deferred basis, offering a unique savings component within the insurance policy itself.

The primary advantage of permanent life insurance lies in its long-term stability and potential for financial growth. It acts as a cornerstone in a comprehensive financial plan, offering both protection and a potential asset for your estate.

The Role of Cash Value

The cash value component is what truly distinguishes permanent life insurance. As you pay your premiums, a portion goes towards the death benefit, while another portion contributes to this cash value. This fund accumulates over time, providing a living benefit that policyholders can access during their lifetime.

Accessing the cash value can be done in several ways, including taking policy loans or making withdrawals. Policy loans typically do not trigger immediate taxation as long as the policy remains in force. Withdrawals, however, can reduce the death benefit and may be taxable if they exceed the premiums paid into the policy. This flexibility makes cash value a valuable resource for various financial needs, from covering unexpected expenses to supplementing retirement income.

Whole Life Insurance: A Traditional Foundation

Key Characteristics of Whole Life

- Fixed Premiums: Premiums remain constant for the entire life of the policy, offering predictability in budgeting.

- Guaranteed Cash Value Growth: The cash value grows at a contractually guaranteed rate, providing a predictable accumulation path.

- Guaranteed Death Benefit: The death benefit is fixed and guaranteed to be paid to your beneficiaries, assuming premiums are paid.

- Potential for Dividends: Many mutual whole life insurance companies pay non-guaranteed dividends, which can increase cash value or reduce future premiums. These are not guaranteed, but can be a pleasant bonus.

Whole Life insurance is often considered the most conservative type of permanent life insurance. It prioritizes stability and guarantees over aggressive growth, making it suitable for those who value certainty in their financial planning.

Benefits of Whole Life

- Predictability and Stability: The guaranteed premiums, cash value growth, and death benefit offer peace of mind.

- Long-Term Wealth Accumulation: Consistent, albeit modest, cash value growth can serve as a dependable savings vehicle over decades.

- Estate Planning Advantages: The guaranteed death benefit provides a reliable way to transfer wealth, cover estate taxes, or create an inheritance.

- Tax-Deferred Growth: Cash value grows without annual taxation, and policy loans can be tax-free.

The simplicity and guarantees of Whole Life make it a favored choice for individuals seeking a secure financial foundation without exposure to market volatility. It acts as a stable asset in a diversified portfolio.

Drawbacks of Whole Life

- Higher Premiums: Whole Life policies typically have higher initial premiums compared to other permanent life insurance options.

- Lower Growth Potential: While guaranteed, the cash value growth rate is generally lower than market-linked investment returns.

- Less Flexibility: Once established, it offers less flexibility in adjusting premiums or death benefits compared to other policy types.

For those looking for higher growth potential or more adaptable premium structures, the fixed nature of Whole Life might be a limitation. However, its stability remains its core strength.

Indexed Universal Life (IUL) Insurance: Market-Linked Potential

Key Characteristics of IUL

- Flexible Premiums: Policyholders can adjust premium payments within certain limits, offering more financial flexibility.

- Cash Value Linked to Market Index: The cash value growth is tied to the performance of a specific stock market index, such as the S&P 500, without directly investing in the market.

- Participation Rates, Caps, and Floors: Growth is subject to a cap rate (maximum interest credited) and a floor rate (minimum interest, often 0% or 1%), providing a balance between growth potential and downside protection. A participation rate dictates what percentage of the index’s positive performance is credited to the policy.

- Adjustable Death Benefit: The death benefit can be increased or decreased over time, offering adaptability to changing life circumstances.

IUL insurance aims to offer the best of both worlds: the potential for higher returns linked to market performance, coupled with the security of a guaranteed minimum interest rate. This makes it an attractive option for those seeking more dynamic growth within a life insurance vehicle.

Benefits of IUL

- Higher Growth Potential: The cash value can potentially grow at a faster rate than Whole Life policies, mirroring market gains up to the cap.

- Protection Against Market Downturns: The floor rate ensures that the cash value will not lose money due to negative market performance, although it might not earn anything in such periods.

- Premium and Death Benefit Flexibility: Policyholders can adjust their payments and coverage as their needs evolve, which can be beneficial for long-term financial planning.

- Tax Advantages: Similar to Whole Life, cash value grows tax-deferred, and loans are typically tax-free.

The flexibility and potential for greater cash value accumulation make IUL a compelling choice for individuals comfortable with a moderate level of market exposure and a desire for adaptable insurance. For more information on index performance, one might consult financial news outlets like Bloomberg or The Wall Street Journal.

Drawbacks of IUL

- Complexity and Fees: IUL policies can be more complex to understand due to various moving parts like caps, floors, and participation rates. They also often come with higher fees and charges.

- Market Caps Limit Upside: While protected from losses, the cap rate limits how much the cash value can earn, even if the underlying index performs exceptionally well.

- Not a Direct Market Investment: It’s crucial to remember that IUL is an insurance product, not a direct stock market investment. You do not own the index funds.

- Potential for Policy Lapse: If premium payments are insufficient to cover policy charges, especially during periods of low index performance, the policy could lapse.

The complexity and need for active management in an IUL policy require a higher level of understanding and commitment from the policyholder. Careful monitoring is essential to ensure the policy remains adequately funded.

Whole Life vs. IUL: A Direct Comparison

Guarantees vs. Market Potential

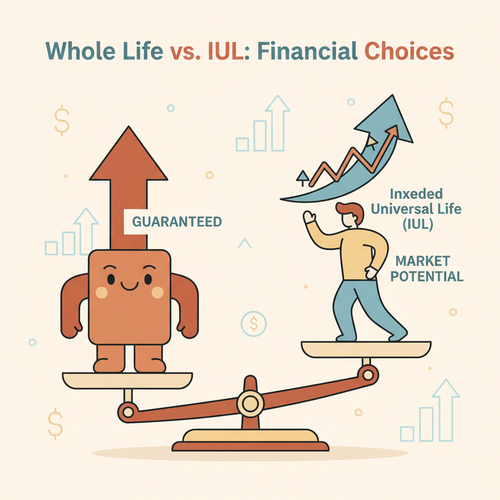

This is perhaps the most significant distinction. Whole Life offers certainty with guaranteed cash value growth and a fixed death benefit. It’s a conservative choice for those who prioritize predictability. In contrast, IUL introduces an element of market-linked growth, offering higher potential returns but without the same level of guarantees on the growth rate. It provides a safety net with its floor, but actual returns are variable.

Premium Structure and Flexibility

Whole Life premiums are rigid and fixed, making budgeting straightforward but less adaptable to changes in income. IUL, on the other hand, provides premium flexibility, allowing policyholders to adjust payments. This can be a double-edged sword, requiring careful management to avoid underfunding the policy.

Cash Value Growth and Access

The cash value in Whole Life grows steadily at a guaranteed rate. This predictable accumulation makes it a reliable long-term savings vehicle. For IUL, cash value growth is tied to an external index, meaning it can experience periods of higher growth and periods of minimal or zero growth, though protected from losses by the floor. Both policy types offer similar access methods to their cash value through loans and withdrawals, but the growth drivers are distinct.

Fees and Transparency

Generally, Whole Life policies are more transparent in their fee structure, often having a more straightforward breakdown of costs. IUL policies can be more complex, with various fees for cost of insurance, administrative charges, and riders, which can impact the net cash value growth. Understanding these charges is crucial for IUL policyholders.

Risk Profile

Whole Life appeals to individuals with a low-risk tolerance seeking guaranteed outcomes. It provides a conservative growth engine. IUL suits those with a moderate risk tolerance who are comfortable with market-linked performance and the potential for higher returns, balanced by some downside protection. It’s important to assess your personal financial risk profile when considering either option.

Which is Right for You? Making an Informed Decision

Choosing between Whole Life and IUL is a deeply personal decision, influenced by your financial goals, risk tolerance, and time horizon. There is no universally “better” option; rather, it’s about finding the policy that best fits your individual circumstances.

- Consider Whole Life if:

- You prioritize guarantees and predictability in your financial planning.

- You prefer fixed premiums and a straightforward policy structure.

- You have a low-risk tolerance and seek stable, consistent cash value growth.

- You value long-term financial security and estate planning above aggressive market-linked returns.

- Consider IUL if:

- You are comfortable with some market exposure for potentially higher cash value growth.

- You desire premium and death benefit flexibility to adapt to changing life stages.

- You have a moderate risk tolerance and understand the implications of caps, floors, and participation rates.

- You are seeking a policy that offers both protection and the potential for more dynamic wealth accumulation.

Regardless of your inclination, the complexity of these products necessitates expert guidance. Consulting with a qualified financial advisor is paramount. They can help analyze your specific situation, clarify policy details, and guide you towards the most suitable option. Resources from organizations like the National Association of Insurance Commissioners (NAIC) can also provide valuable consumer information.

Conclusion

Both Whole Life and Indexed Universal Life insurance policies offer significant advantages as tools for both insurance coverage and wealth building. Whole Life provides a bedrock of guarantees, predictable growth, and unwavering stability, appealing to the conservative planner. IUL, conversely, offers the allure of market-linked growth potential, balanced by downside protection and greater flexibility, suiting those with a higher appetite for dynamic returns within an insurance wrapper.

Ultimately, the “better” choice is the one that aligns most closely with your personal financial philosophy, your long-term objectives, and your comfort level with risk. Understanding the nuances of each policy is the first step. The next crucial step is to engage with a financial professional who can translate these concepts into a tailored strategy for your financial success and peace of mind.