Understanding APY vs. APR is fundamental for new investors. Indeed, these two acronyms heavily influence your savings’ growth and borrowing costs. Therefore, grasping their distinctions is vital for sound financial decisions. Consequently, this comprehensive guide will clarify both terms. We will extensively explore how they significantly affect your money.

What is APR? Decoding the Annual Percentage Rate

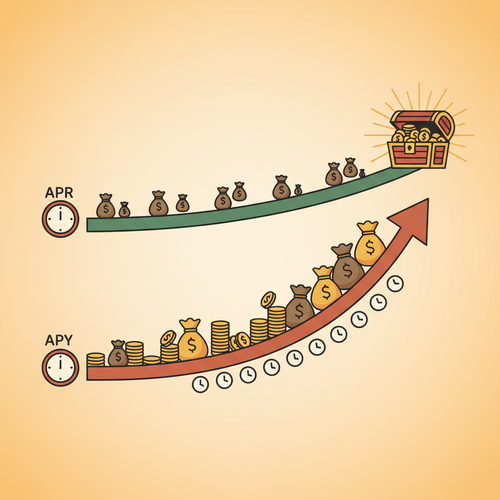

APR stands for Annual Percentage Rate. Essentially, it represents the yearly cost of borrowing money or the yearly rate charged for extending credit. Lenders typically use APR for various types of loans. For instance, credit cards, auto loans, and mortgages often cite an APR prominently. Moreover, it usually reflects the simple interest rate. This specific calculation means interest is primarily calculated only on the principal amount borrowed.

Furthermore, APR does not inherently account for the effect of compounding interest in its most common form. Thus, the stated percentage is generally what you expect to pay annually on the principal. However, some loans might include certain fees and charges within their APR calculation. Specifically, these additional fees can incrementally increase the overall borrowing cost you face. Therefore, always read the fine print carefully and ask questions to fully understand the APR. Understanding APR is crucial for accurately evaluating loan costs.

What is APY? Unpacking the Annual Percentage Yield

Conversely, APY means Annual Percentage Yield. This term is absolutely crucial for understanding your savings potential. Specifically, APY reveals the actual rate of return an investment or savings account will earn over a year. It explicitly includes the powerful effect of compounding interest. Compounding means earning interest not only on your initial deposit but also on all the accumulated interest from previous periods.

Consequently, APY almost always looks slightly higher than the stated nominal interest rate. Indeed, this difference arises because of the consistent power of compounding over time. For instance, a savings account advertising a 1.00% nominal interest rate might actually boast a 1.004% APY. This happens if interest compounds monthly, daily, or even more frequently. Therefore, APY gives a more accurate and comprehensive picture of your money’s true growth potential.

The Core Difference: Compounding’s Impact

Why Compounding Matters for Your Money

The most significant and defining distinction between APY and APR lies squarely in the concept of compounding. APR typically ignores its amplifying effect on the interest charged or earned. However, APY fundamentally embraces and highlights this powerful financial concept, showcasing its benefit. Consequently, a higher APY consistently translates into faster and more substantial wealth accumulation for savers. This advantage is especially true and pronounced for those with long-term savings goals.

Specifically, imagine comparing two hypothetical savings accounts. One offers a 2% APR, which might be a simple interest rate. The other account, however, boasts a 2% APY, indicating compounding. The APY account will unequivocally yield more money over the same period. This positive outcome happens because your previously earned interest also starts earning interest, creating an exponential growth effect. Therefore, compound interest is often aptly called “interest on interest.” It truly supercharges your savings, making your money work harder for you.

APY in Action: Growing Your Savings

Maximizing Returns with High APY Accounts

When considering various savings products, savvy investors always prioritize the APY. For example, high-yield savings accounts prominently highlight their APY to attract depositors. Certificates of Deposit (CDs) also explicitly display their APY, representing the total return over their term. Furthermore, many money market accounts extensively use APY to showcase their competitive rates to potential clients. Indeed, a higher APY directly means your deposited money works significantly harder for you, growing more quickly.

Specifically, it is prudent to meticulously compare different financial institutions’ offerings. Always look beyond merely the advertised nominal interest rate. Instead, strategically focus your attention on the Annual Percentage Yield, as it reveals the true growth. Consequently, even a seemingly small difference in APY can cumulatively lead to substantial financial gains over time. This effect becomes particularly noticeable and impactful over several years. Therefore, smart and informed savers consistently chase the best available APY to optimize their returns.

APR in Action: Understanding Borrowing Costs

Minimizing Loan Expenses with Low APR

Conversely, when contemplating borrowing money, you should always strive for the lowest possible APR. For instance, credit cards notoriously carry high APRs, which can quickly lead to substantial debt if not managed carefully. Personal loans and auto loans also prominently carry an APR, indicating their yearly cost. A lower APR directly translates to less money paid in overall interest charges throughout the loan’s life. Therefore, comparing APRs extensively is absolutely essential before taking out any type of loan.

Furthermore, mortgage rates are frequently quoted as an APR. This comprehensive figure typically includes the stated interest rate plus certain associated closing costs and fees. Consequently, it aims to provide a clearer and more complete picture of the loan’s total cost to the borrower. However, always make sure to ask about all associated fees, charges, and conditions. Specifically, ensure no hidden charges exist that could unexpectedly inflate your borrowing expenses. Ultimately, understanding APR empowers you to borrow responsibly and economically.

Real-World Scenarios: APY vs. APR Examples

Savings Accounts and CDs

- High-Yield Savings: These accounts invariably show their APY. A 2.00% APY means you effectively earn 2% per year on your balance, including the consistent compounding.

- Certificates of Deposit (CDs): CDs lock in your money for a set term, offering a guaranteed return. They also prominently advertise their APY, reflecting the true total return over the certificate’s duration. Therefore, a 1-year CD with a 3.00% APY will undeniably grow your principal by that precise amount annually.

Loans and Credit

- Credit Cards: Credit cards universally have an APR. A 19.99% APR signifies you will pay nearly 20% on your outstanding balance annually, though this can compound if not paid off monthly.

- Mortgages: Mortgage lenders typically quote an APR. This important figure includes the principal interest rate plus certain specific closing costs, such as discount points or lender fees. Consequently, it genuinely gives a more transparent and comprehensive picture of the loan’s overall total cost.

Understanding these practical real-world applications helps you make consistently informed financial choices. Specifically, always remember this guiding principle: seek high APY for your valuable savings. Conversely, diligently aim for low APR when you need to borrow money. This simple yet powerful rule effectively guides many successful financial decisions throughout your life.

Tips for Beginner Investors: Navigating APY and APR

Making Smart Financial Decisions

Navigating complex financial terms can often seem daunting for newcomers. However, mastering the fundamental difference between APY vs. APR provides an incredibly strong foundation. Consequently, here are some actionable and practical tips specifically designed for beginners. These insights will undoubtedly help you optimize your personal financial journey and build wealth effectively.

First, always meticulously compare the APYs for all potential savings products. Do not just look at the stated nominal interest rate in isolation. Indeed, the consistent compounding effect truly makes a significant and measurable difference over time. Furthermore, always check the compounding frequency offered by the institution. Daily or monthly compounding is demonstrably better than annual compounding, allowing your money to grow more rapidly and consistently. Specifically, institutions might offer similar initial interest rates but varying compounding periods, which significantly impacts your overall return. Therefore, this seemingly small detail truly matters for maximizing your long-term wealth accumulation.

Second, rigorously scrutinize the APRs for all loans you consider. A lower APR unequivocally means less money out of your pocket over the entire loan’s duration. Specifically, diligently explore options from different lenders, including traditional banks, credit unions, and various online providers. This diligent and comprehensive comparison can potentially save you thousands over the loan’s lifetime. Therefore, always shop around meticulously and negotiate before committing to any borrowing agreement. Understanding the full and true cost of borrowing thoroughly empowers you to make better financial choices.

Third, diligently build and maintain an emergency fund. Keep this essential money securely held in a high-APY savings account. This prudent approach ensures your financial safety net grows steadily, rather than simply sitting idle and losing purchasing power to inflation. Furthermore, make it an absolute priority to avoid carrying credit card balances month-to-month. High APRs on credit cards can quickly and drastically erode your finances, creating a challenging cycle of debt. Consequently, prioritizing prompt debt repayment, especially high-interest debt, is always a wise and financially sound move.

Fourth, seriously consider your long-term financial goals and aspirations. Compound interest truly shines and demonstrates its power over extended periods, turning even modest initial contributions into substantial sums. Therefore, make a concerted effort to start saving and investing early, even if the amounts seem small initially. Even small, consistent contributions can grow substantially with a consistently good APY. Financial literacy and proactive planning are indeed your greatest assets for long-term prosperity and security.

Fifth, make a commitment to educate yourself continuously on all financial matters. The financial landscape constantly evolves, introducing new products, regulations, and investment strategies. Resources from reputable institutions offer invaluable insights into managing your money effectively and staying informed. Reuters and Bloomberg provide excellent economic news, market updates, and global financial analysis. Additionally, exploring reliable sites like The Wall Street Journal, Investopedia, and the Federal Reserve offers expert analysis, educational content, and crucial regulatory information. Specifically, this continuous knowledge acquisition consistently empowers you to make increasingly better and more confident financial decisions throughout your life.

Finally, review your financial accounts regularly and diligently. Ensure you are consistently getting competitive rates on both your savings products and any borrowing you undertake. If not, critically consider switching banks or exploring new financial products that offer demonstrably better terms and conditions. This proactive and engaged approach keeps your money working hard for you, preventing stagnation and maximizing your financial potential. Ultimately, a deep understanding of APY and APR is a foundational cornerstone of robust financial health and enduring well-being.

Conclusion

In conclusion, differentiating APY from APR is not merely an academic exercise. It holds profound practical and far-reaching implications for your hard-earned money and your financial future. Specifically, APY precisely dictates how much your savings will genuinely grow over time, thanks to the magic and consistent power of compounding. Conversely, APR accurately determines the true and total cost of your borrowing endeavors, from credit cards to mortgages. Therefore, making consistently informed financial choices inherently means recognizing and effectively applying these crucial distinctions in your daily financial life.

For beginner investors, cultivating this essential understanding is absolutely paramount for long-term success. Make it a steadfast habit to seek out the highest possible APY for all your deposits, whether placed in savings accounts, money market accounts, or Certificates of Deposit. Conversely, always strive for the lowest possible APR on any loans you acquire, diligently comparing offers. By consistently doing so, you effectively harness the powerful force of compounding to your significant financial benefit. Consequently, you actively build a stronger, more resilient, and prosperous financial future for yourself and your loved ones. Always remember: robust financial knowledge truly is enduring power in the intricate and dynamic world of personal finance.